The not-for-profit recently reported its financial results for the second quarter of its fiscal year 2024, and there are several reasons CFOs should care.

CommonSpirit Health’s latest earnings report shows a significant improvement in financial performance compared to the prior year, driven by higher volume levels, efficiency initiatives, and a reduction in length-of-stay.

However, the health system continues to face challenges such as salary and supply cost inflation outpacing payer reimbursement rates and an increasing rate of denials from some payers.

So how did these improvements and challenges affect CommonSpirit’s overall performance and why should CFOs take note? Let’s take a look.

The numbers

The health system reported operating revenues of $9.35 billion and operating expenses of $9.44 billion for the quarter ended Dec. 31, 2023, compared to $8.19 billion in revenues and $8.63 billion in expenses for the same period last year.

The operating loss was $87 million, with EBITDA of $484 million, resulting in an operating margin of -0.9% and an EBITDA margin of 5.2%, both normalized for the California provider fee program.

This marks a significant improvement from the prior year, where the EBITDA margin was only 0.6%.

The analysis

One key driver of the improved financial performance was an increase in volumes, with adjusted admissions rising by 6.9% and outpatient visits increasing by 3.3% in the second quarter. Additionally, efforts to reduce the average length of stay from 4.98 days to 4.77 days have contributed to the financial improvement.

Despite these positive trends, CommonSpirit continues to face challenges, particularly in managing the impact of inflation on costs and dealing with an increasing rate of denials from certain payers.

According to the report, the health system is working closely with health plans to reduce prior authorization denials and speed up reimbursement processes.

Additionally, CommonSpirit is expanding its ambulatory footprint, enhancing workforce retention programs, and identifying programs to further establish its essentiality in the communities it serves.

CFO Dan Morissette acknowledged the progress made in improving financial performance but emphasized that there is still work to be done.

In the earnings report, he highlighted the health system's focus on exploring growth opportunities, implementing a sound investment strategy, and containing costs to further improve financial performance.

Morissette also emphasized the importance of providing essential care and services to the communities served by CommonSpirit.

Why should other CFOs care?

There are several key strategies from CommonSpirit's earnings report that can help CFOs boost their own performance.

First, it’s obvious that focusing on volume growth and efficiency initiatives can have a positive impact on financial performance. Keep prioritizing efforts to reduce length-of-stay and manage the continuum of care to help improve margins and operating results.

Second, CFOs should continue to be vigilant about managing costs in the face of inflationary pressures, even as numbers start to ease. Pay close attention to salary and supply cost inflation and work to contain costs where possible to prevent them from outpacing reimbursement rates.

Lastly, engage with payers to address denials and reimbursement delays. Collaborate with health plans to reduce prior authorization denials and streamline reimbursement processes to ensure timely payments for services provided.

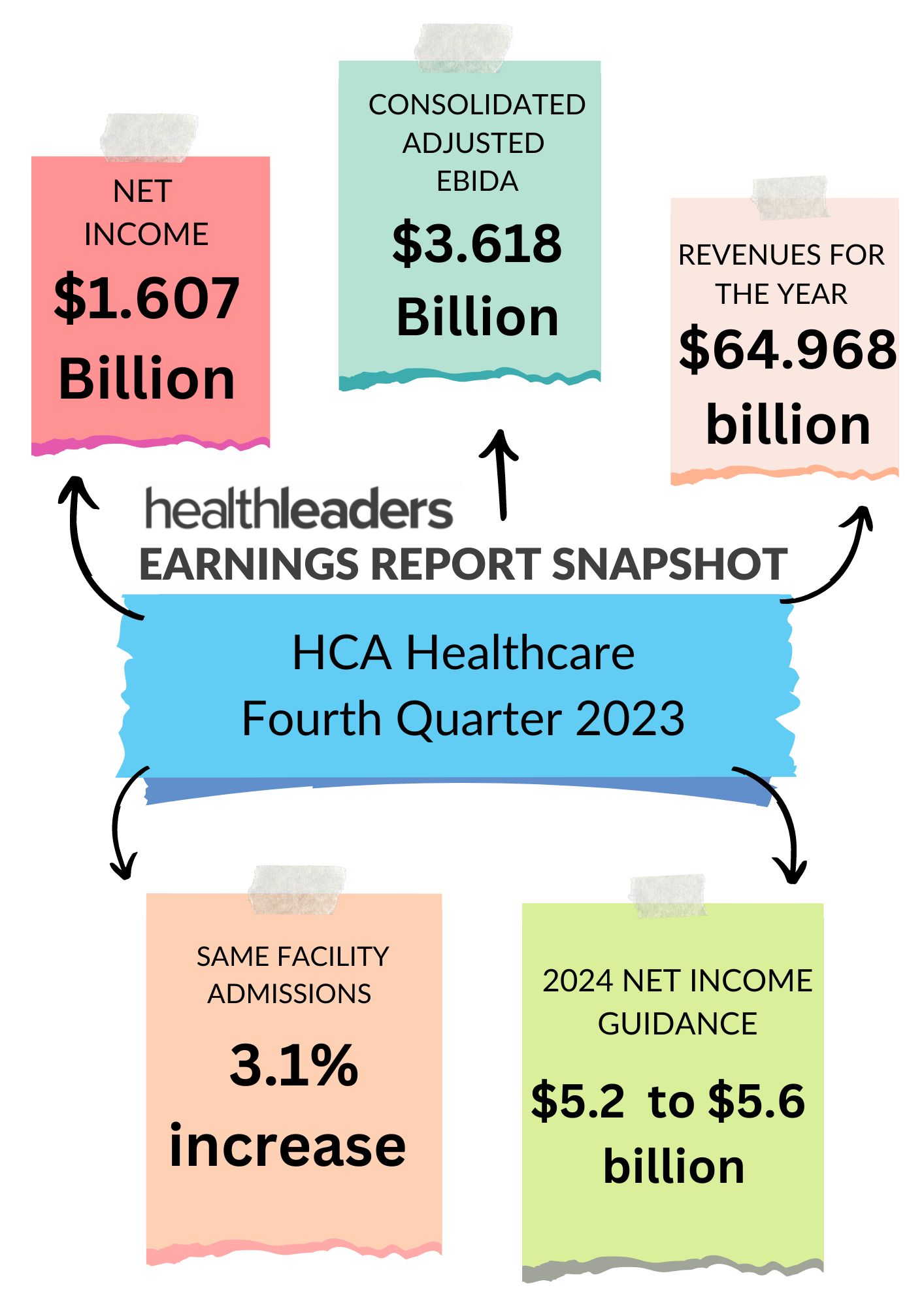

HCA Healthcare reported solid financial performance in the fourth quarter of 2023, driven by strong demand for services across their portfolio of markets, facilities, and service lines.

Here is a snapshot of what HCA reported in the fourth quarter of 2023.

CFOs are feeling optimistic about the financial outlook, but there are three large challenges that will need to be navigated.

A majority (79%) of healthcare CFOs expect a revenue increase this year, yet 78% cited profitability as an area of improvement, according to a healthcare CFO outlook survey conducted by BDO.

While CFOs remain optimistic, BDO warns that healthcare organizations may face challenges in achieving higher revenue and profitability due to three main reasons: regulatory pressures, clawbacks of COVID-19 funding, and challenging bond and loan covenant agreements.

A look at the numbers

The survey, which included responses from 100 CFOs, found that 11% of respondents reported their organizations had violated bond and/or loan covenants in the past year, and 30% expressed concern about violating them in the future.

Furthermore, only 35% of healthcare organizations represented in the survey had more than 60 days cash on hand. This highlights the need for more strategic conversations around economic resilience, as identified by 44% of CFOs.

What’s the solution?

In response to these challenges, CFOs are shifting their strategies.

The survey found that 39% of CFOs are adjusting revenue cycle management to improve liquidity, while 37% are engaging in strategic cost reductions, including staff. Another 34% are focusing on transforming operating models. These approaches reflect the need for cash flow optimization, cost optimization, and risk management to ensure the continuity of care for patient communities.

Efforts to optimize revenue cycles through roles and workflows, denials, and post-payment audits, as well as the implementation of AI and robotic process automation, are also expected to increase efficiency and financial performance, the survey noted.

Dealmaking is also a priority for healthcare CFOs this year, with nearly three-quarters of respondents including it on their to-do lists. However, challenges such as navigating due diligence, finding the right target or buyer, and addressing valuation gaps are still top concerns for healthcare finance leaders.

What about investments?

CFOs are starting to recognize the potential of new advancements in AI, particularly generative AI.

Almost half (47%) of surveyed CFOs expect to increase technology implementation spending this year, with 98% piloting generative AI and 46% building a proprietary generative AI platform.

These investments are focused on improving front- and back-office operations, including digital investments in patient-provider communications and remote patient care. Use cases for generative AI include treatment plan generation, clinician-to-patient communications, and diagnostics and medical imaging.

In addition to AI, CFOs are investing in predictive staffing, financial reporting software, and enterprise data analytics to enhance their organizations' performance and financial decision-making capabilities.

What does it all mean?

Overall, the survey highlights the cautious optimism of healthcare CFOs for the financial outlook of their organizations in 2024.

While there are challenges to be addressed, CFOs are taking a proactive approach by revisiting strategies and making investments in revenue cycle management, cost optimization, and technology. By focusing on cash flow, efficiency, and risk management, CFOs aim to ensure the continuity of care and resiliency of their operations.

Tenet beat Wall Street expectations by a hefty amount in the fourth quarter of 2023.

Tenet Healthcare recently reported impressive results for the quarter and year ended December 31, 2023, beating Wall Street expectations.

The company's net income in the fourth quarter of 2023 was $244 million, compared to $102 million in the same period of 2022. This significant increase in net income is attributed to strong same facility revenue growth and disciplined operating management.

But How Did Tenet Pull it Off?

Tenet's adjusted EBITDA, excluding grant income, for the fourth quarter of 2023 was $1.010 billion, compared to $857 million in the fourth quarter of 2022. This growth is driven by strong volume growth in the ambulatory care and hospital operations segments, favorable payer mix, and improved contract labor costs, the report said.

As HealthLeaders has been reporting, focusing on a favorable payer mix and lowering those contract labor costs has been key for CFOs looking to improving margins.

Additionally, the company recognized a $52 million aggregate favorable pre-tax impact associated with Medicaid supplemental revenue program adjustments in California and Texas.

It’s also worth noting Tenet’s COVID-related stimulus grant income. In the fourth quarter of 2023, Tenet received $2 million pre-tax ($2 million after-tax) in grant income, while in the same period of 2022, it received $40 million pre-tax ($30 million after-tax).

The company's balance sheet and cash flows also showed positive trends.

Cash flows provided by operating activities for the year ended December 31, 2023, were $2.374 billion, compared to $1.083 billion in the previous year. Tenet produced free cash flow of $1.623 billion in 2023, compared to $321 million in 2022.

This increase in cash flows highlights the company's strong financial performance and ability to generate cash, something that a lot of CFOs have been battling so far in 2024.

Significant business transactions

Tenet also made noteworthy transactions recently.

It completed the sale of three hospitals and related operations in South Carolina to Novant Health for approximately $2.4 billion. Additionally, the company signed a definitive agreement to sell four hospitals and related operations in Orange County and Los Angeles County, California, to UCI Health for approximately $975 million.

These transactions are expected to result in pre-tax book gains, reducing the company's income tax expense in 2024 by approximately $190 million due to a reduction in interest expense limitations.

In terms of its business segments, Tenet's ambulatory care segment, which includes United Surgical Partners International, saw a 15.4% increase in net operating revenues in the fourth quarter of 2023 compared to the same period in 2022.

This growth is driven by strong same-facility net surgical case growth, acquisitions, opening of new facilities, service line growth, and improved pricing yield the earnings report says.

Tenet's hospital operations and services segment, primarily consisting of acute care and specialty hospitals, also reported positive results.

Net operating revenues increased by 6.0% in the fourth quarter of 2023 compared to the same period in 2022, mainly due to increased adjusted admissions, favorable payer mix, and improved pricing yield.

The segment's adjusted EBITDA, excluding grant income, was $546 million in the fourth quarter of 2023, compared to $450 million in the same period of 2022.

What it all means

Overall, Tenet's earnings report highlights its overall positive performance in 2023, driven by strong revenue growth and effective operational management.

CFOs understand the importance of disciplined operating management, prudent financial decisions, and strategic investments in technology and ambulatory care—and Tenet was a pretty good example of this in 2023.

A strong, collaborative relationship with payer partners is essential for one CFO.

At a time when providers can feel like they are at a crossroads with payers, Bridgett Feagin, CFO for Connecticut Children's—a level 1 pediatric trauma center with roughly $600 million in net patient revenue—says building a strong relationship with payers is the key to reducing administrative burdens and denials, and ensuring payment.

But how it is done? Leveraging its payer mix, putting pressure on its commercial payers, and keeping communication open has been key Feagin previously told HealthLeaders.

“It's a collaborative relationship, meaning that [payers] understand our needs and we also understand their business needs as well. So, if it costs $100 to take care of this patient, we at least need to cover our costs,” Feagin said.

Connecticut Children's is a payer mix with close to 60% of Medicaid, and Medicaid does not cover Connecticut Children's costs, Feagin says.

“So, we need our commercial payers to give us a little bit more than the costs. So, we can shift some of that liability over to our commercial payers. And that's just the way it works. They understand that but we are working with the state as well to increase our reimbursement to cover our costs,” Feagin says.

Feagin also explained that a good payer partnership also reduces administrative burdens, such as a denial. “When a payer denies a claim, it creates more administrative work for my team. On the front end, we're talking to payers about what we need to do, to make sure we don't get a denial in the first place.”

But how can you collaborate to ensure that a claim won't be denied?

Having monthly team meetings and keeping communication open with the payers helped ensure claims don’t get denied she says.

“One example would be with our NICU babies. Typically, we're supposed to notify our payers within 48 hours, that the baby is admitted to the hospital,” Feagin said. “However, those parents are not thinking about providing the information, because they have a critically ill child that's been admitted to the ICU.”

“We need to be compassionate and work with the family to get the information and find out who their insurance company is. Sometimes that takes over 48 hours. So, say if it goes to 72 hours, we'll contact the payer and say we'll have this information beyond the 48 hours,” Feagin says.

“Now they'll have it in their system, and they get the authorization done. So that's an example of working with the payer to make sure we don't get a denial on the back end.”

As CFOs fight against poor margins, a new study is showing that hospitals and health systems are increasingly pursuing M&A to stabilize their financial situation, which is partly driving more dealmaking.

But what exactly are the numbers saying? Check them out below and read the full story on the Kaufman Hall report here.

The payer/provider turmoil has been heating up, and now there are numbers to show that it's not just all in our heads.

A not-so-unexpected trend has emerged: a notable uptick in payer/provider disputes year over year.

In addition, according to research by FTI Consulting, disagreements over reimbursement rates and contract terms have also garnered more media attention in the last year, consistent with what HealthLeaders has been reporting.

Even more, among these payer/provider disputes there seems to be a clear opponent for providers: Medicare Advantage (MA).

Let’s look at what it all means and how CFOs can better address these challenges.

The numbers

According to the research, over the past two years negotiations between payers and providers have increasingly resulted in disputes that have captured the attention of the media. The coverage of these disputes has grown significantly, with a remarkable increase in 2023 compared to the previous year.

The study found that in 2023, there were 86 publicly reported disputes covered by media outlets, showing a 69% surge from the 51 disputes witnessed in 2022. These conflicts have spanned across 34 states, emphasizing the widespread impact.

"I think you're going to see an acceleration in the public town square, the competitiveness and the negotiating in the public opinion space," Britt Berrett, managing director and teaching professor at Brigham Young University and former CEO with HCA, Texas Health Resources, and SHARP, previously told HealthLeaders.

"I think moving forward, you're going to see a tremendous amount of public awareness on contract negotiations. Payers and providers are going to be arguing their cases in the town square," he says.

Interestingly, out of the total disputes covered by the media in 2023, 44% failed to reach an agreement. This failure to establish timely agreements mirrors the trend observed in 2022 when 45% of disputes remained unresolved.

In 2023, 59% of the disputes reported in the media involved MA plans, with 12 disputes exclusively focused on MA plans. This trend aligns with the previous year, where 56% of disputes referenced MA plans.

What does it mean for hospital and health system CFOs?

We know that payer/provider relationships are only becoming more complex, and these disputes are starting to take center stage among the challenges faced by hospital and health system CFOs.

The surge in media coverage of these differences underscores the need for proactive measures to navigate the evolving payer landscape.

Here are key strategies I have gathered from some of the best CFOs in the game:

Strengthen negotiation tactics: As reimbursement rates become a more contentious issue, CFOs need to enhance their negotiation strategies to secure favorable agreements with payers.

And CFOs need to remember they have more leverage in negotiation talks than they think, but it requires willingness and preparation to pull levers that may be uncomfortable yet necessary for financial survival.

One option is to collaborate with legal and financial teams to develop a well-informed bargaining position can help ensure fair reimbursement.

A second option? Consider contact termination.

Dropping a payer is “absolutely an important strategy,” Berrett says. “Providers are becoming more capable in measuring the impact of the slow or rejected payments, and providers are looking at the actual cost of care by patient. Payers need to be aware that.”

There are two important considerations for providers when negotiating, Berrett says. “Are we able to collect our negotiated rates, and are the patients covered by this payer more expensive to treat?”

Develop robust communication channels: Establishing effective lines of communication with payers is crucial to resolving disputes promptly. CFOs should work closely with their revenue cycle management teams to foster open dialogue with payers, enabling timely negotiation and dispute resolution.

Focus on your patient impact: Hospital and health system CFOs must prioritize patient experience and minimize disruption amidst disputes. Developing contingency plans and early communication with patients can alleviate concerns and ensure seamless access to care.

Monitor the regulatory environment: Stay abreast of regulatory changes and proposed legislation that may impact payer-provider relationships—for example, CMS’ attempt to better regulate MA. Understanding evolving regulations can inform negotiation strategies and help CFOs navigate potential roadblocks.

Reducing labor costs is a top concern for CFOs, especially since the money CFOs pumped into contract labor during the pandemic is now majorly stressing the bottom line.

Changes in the workforce landscape are forcing CFOs to be more creative, meaning many are looking toward AI to fill workforce gaps and optimize processes.

But is it the answer to this crisis? It will probably take more time for healthcare leaders to rely on generative AI.

According to PricewaterhouseCoopers’ (PwC) annual global survey, which interviewed 4,702 CEOs across the world, it found that healthcare leaders are less likely to turn to generative AI than those in most other industries.

As HealthLeaders reported, the findings underscore AI’s growing presence in businesses, but also healthcare’s tepid willingness to fully invest in the technology right now—even amid heightened workforce challenges.

When looking at this data from a healthcare CFO’s perspective, it’s not surprising AI has had a slower roll out as every financial decision needs to be weighed very carefully—and as we know healthcare is a very complicated market with a lot at stake.

But, that’s not to say AI hasn’t already taken off for some CFOs.

In fact, Stephen Forney, SVP and CFO of Covenant Health, told HealthLeaders AI plays an important part in ensuring the organization’s financial stability and alleviating staff burdens.

“At Covenant, we've seen how AI can play a crucial role in addressing financial challenges by streamlining workflows and improving revenue cycle management,” he says.

Covenant also leverages an automated philanthropic aid platform that helps keep them up to date on the latest aid programs, alerts them when they're open for enrollment, and helps match its patients to the program they're best suited for, streamlining the process significantly for all stakeholders Forney says.

“Integrating AI into our systems promotes efficient resource utilization and better financial outcomes,” Forney says.

So what are your thoughts? Is your organization proceeding with caution when it comes to AI?

The financial outlook for not-for-profit hospitals and health systems is once again under scrutiny.

With operating margins at risk of a permanent reset, concerns have been raised among investors as it may lead to widespread downgrades, a new report by Fitch Ratings says.

While we are not expected to face a "sector-ending incident," hospitals and health system CFOs must carefully manage their liquidity and capital spending to navigate these challenges.

What is Happening with Operating Margins?

Traditionally, healthy operating margins for hospitals have ranged from 3% or higher.

In fact, even Kaufman Hall has reported that the median calendar year-to-date operating margin index was 2.0% through the end of this past November, “still well below the 3%-4% range often cited as a sustainable operating margin for not-for-profit hospitals and health systems.”

Now, Fitch Ratings predicts that the ideal range will likely reset to 1%-2% for not-for-profit hospitals in the future. While a significant reduction, the report suggests that widespread downgrades are unlikely due to the robust balance sheets and capital spending discipline demonstrated by many health systems.

Despite this, individual hospitals may face downgrades if they are unable to defer capital investments and fail to improve operational efficiencies.

What is the Cause?

One of the critical factors contributing to the financial uncertainty ahead is the aging population Fitch says.

By 2030, the last of the baby boomer generation will reach the age of 65, leading to a larger population in need of heightened healthcare services.

This scenario may strain healthcare providers' resources, potentially impacting their profitability. The need for increased staffing and the associated costs, the report says, may offset any gains made in operational efficiencies.

Another area of concern in the report is the days' cash on hand ratio. It questions whether the current range of 200-250 days may be too high, given the ongoing struggles of the sector.

However, the data shows that the ratio has consistently remained above 200 days in nine out of the last ten years, with a median of 216 days based on 2022 financials. Despite potential improvements in profitability and investment gains, the report suggests that this metric may see little improvement.

So how can CFOs prepare?

There are a few strategies hospital and health system CFOs can use to stay ahead.

Maintain a robust balance sheet: The report highlights the importance of building and maintaining a robust balance sheet to withstand potential financial challenges. CFOs should focus on healthy liquidity cushions to protect against unforeseen circumstances and maintain financial stability.

Optimize capital spending: As the industry faces financial headwinds, CFOs should evaluate capital spending carefully. Prioritizing investments that directly contribute to operational efficiency and improved patient care will be crucial to ensure long-term success.

Plan for the aging patients: With the incoming surge of the baby boomer generation requiring increased healthcare services, CFOs must develop strategic plans to support the growing demand. This may include proactive workforce planning, optimizing processes, and leveraging technology to enhance efficiency.

Monitor days' cash on hand ratio: While the current days' cash on hand ratio range may be appropriate given the sector's challenges, CFOs should continue monitoring this metric. A robust ratio can provide a buffer during economic downturns or unforeseen circumstances, safeguarding against potential financial instability.

While moving in a positive direction, the outlook for not-for-profit hospitals and health systems presents challenges that demand careful financial planning and strategic decision-making. While the reset of operating margins and the pressure to improve profitability may not result in widespread downgrades, it is essential for CFOs to maintain strong financial foundations.

This time, CMS is to blame for upsetting Humana's funding expectations for 2025.

CMS recently released its proposed Medicare Advantage (MA) payment rules for 2025—and it includes a 0.2% decrease in average benchmark payment rates for next year.

One payer quick to speak out on the decrease? Humana.

Coming on the heels of a huge fourth quarter loss, Humana says if CMS’ rate changes are finalized as proposed, the MA changes will lower Humana’s benchmark funding by around 160 basis points.

Humana, one of the major players in the MA program, analyzed the proposed rule and found that the changes will lower its funding even though the company had expected rates to stay the same.

The issue revolves around the effective growth rate restatements, which Humana didn't anticipate considering the industry's higher medical cost trends, according to its filing with the SEC.

While this rate decrease would be bad news for Humana, CMS says payers are expected to still make $16 billion more next year compared to this year. Even still, it’s likely payers will lobby for a higher payment rate before the final notice is released in April.

Although MA has historically been lucrative for insurers, recent regulatory changes and rising costs due to increased medical care for seniors are putting the offering at risk.

In fact, while MA is still growing, it is showing signs of becoming less profitable for payers, a report by Moody's said.

We may see an uptick in MA payers raising premiums, reducing benefits, and even considering leaving certain markets to improve their margins—changes that would make providers even less likely to keep their MA contracts.

ffb1.jpg?itok=hFeFDUSt)