Staying abreast of the healthcare finance market is a must for CFOs, and there were four stories that were top of mind for leaders.

Here are the four stories that CFOs tracked in 2023:

Mclaren St. Luke's closed down in 2023 due to 'historical financial losses'

McLaren St. Luke’s, a Maumee, Ohio-based healthcare provider, closed the hospital in the spring following years of declining revenues and an unstable reimbursement environment.

"Despite the tireless dedication of everyone associated with McLaren St. Luke’s, we have not been able to overcome the historic financial losses experienced by this hospital—losses that began long before COVID-19 that now run into the millions each month," Jennifer Montgomery, RN, MSA, FACHE, president and CEO of McLaren St. Luke’s, said in a statement announcing the closure. "Our passion for patient care and commitment to clinical excellence have never wavered. But sadly, we are not on a financially sustainable path."

Steward Health Care System CEO said we would see more VBC in 2023

Steward Health Care Systems prides itself on being a leader in the transition to value-based care (VBC). This Dallas-based operator of 39 hospitals across Arizona, Arkansas, Florida, Louisiana, Massachusetts, Ohio, Pennsylvania, Texas, and Utah generates roughly $6.5 billion in annual revenue and was founded on the VBC model.

CEO Ralph de la Torre, MD, connected with HealthLeaders this year to discuss the organization’s success with the VBC model, why hospitals may be reluctant to adopt a VBC model, and why he thought that would change in 2023.

How CFOs are balancing physician compensation with lowering labor costs

Hospital and health system CFOs are facing a bit of a dilemma when it comes to recruiting and retaining physicians. On one end, physician compensation is rising. On the other, slashing labor costs is a priority.

That reality necessitates that CFOs achieve a balancing act between employing top talent while keeping expenses in check. But hospitals' bottom lines aren't just affected by how much it costs to pay a physician. There are also opportunity costs and other expenses associated with physicians walking out the door in search of better compensation.

For that reason, cutting corners with physician salary isn't at the top of CFOs' to-do list. If anything, the opposite seems to be true, with hospitals acknowledging the competitive landscape for attracting and retaining physicians and showing willingness to invest in their workforce.

Deal Or No Deal: 3 ways CFOs can take a stand in contract negotiations with payers

If it seems like contract negotiations between payers and providers are becoming more adversarial and playing out in public more often, that's not just perception—it's the reality in which the fragmented healthcare system currently operates.

Thanks to economic headwinds made up of record inflation and operational challenges, hospital and health system CFOs find themselves with their backs against the wall in negotiations with insurers. Operating margins may be slowly improving, but they remain razor thin for many, especially in comparison to the profits payers continue to reap.

As contracts agreed upon in a different financial climate reach their expiration, the two sides are being forced to come to the table and find new common ground during a new normal in healthcare.

There are significant cultural and operational differences which will need to be accounted for when making moves in 2024.

CFOs will continue to fight against poor operating margins, reduced reimbursement, and inflated expenses in 2024, developing and executing a strategic path to a financially sustainable future is essential. For some, this can mean an acquisition or merger.

Hospitals and health systems of every type are feeling the financial pressure—even nonprofits will continue to grapple with existential questions about their strategy and structure moving forward.

Realizing the fundamental differences between for-profit and nonprofit hospitals will play a large part in a leader’s decision making.

For-profit and nonprofit hospitals are fundamentally similar organizations with subtly different cultural approaches to managing the economics of healthcare. All acute care hospitals serve patients, employ physicians and nurses as their primary personnel, and operate in the same regulatory framework for delivery of clinical services.

There are, however, a few primary differences between for-profit and nonprofit hospitals, which could potentially impact ROI.

TAX STATUS

The most obvious difference between nonprofit and for-profit hospitals is tax status, and it has a major impact financially on hospitals and the communities they serve.

Hospital payment of local and state taxes is a significant benefit for municipal and state governments, said Gary D. Willis, a former for-profit health system CFO said. The taxes that for-profit hospitals pay support "local schools, development of roads, recruitment of business and industry, and other needed services," he said.

The financial burden of paying taxes influences corporate culture—emphasizing cost consciousness and operational discipline. For example, for-profit hospitals generally have to be more cost-efficient because of the financial hurdles they have to clear.

OPERATIONAL DISCIPLINE

With positive financial performance among the primary goals of shareholders and the top executive leadership, operational discipline is one of the distinguishing characteristics of for-profit hospitals, said Neville Zar, the former senior vice president of revenue operations at Steward Health Care System, a for-profit that includes 3,500 physicians and 18 hospital campuses in four states.

When Zar was at the system, a revenue-cycle dashboard report was circulated at Steward every Monday morning at 7 a.m., including point-of-service cash collections, patient coverage eligibility for government programs such as Medicaid, and productivity metrics.

A high level of accountability fuels operational discipline at for-profits, Zar said.

FINANCIAL PRESSURE

Accountability for financial performance flows from the top of for-profit health systems and hospitals, said Dick Escue, former CIO at a health insurance company. Escue also worked for many years at a rehabilitation services organization that for-profit Kindred Healthcare of Louisville, Kentucky, acquired in 2011. "We were a publicly traded company. At a high level, quarterly, our CEO and CFO were going to New York to report to analysts. You never want to go there and disappoint. … You're not going to keep your job as the CEO or CFO of a publicly traded company if you produce results that disappoint."

Finance team members at for-profits must be willing to push themselves to meet performance goals, Zar said.

For-profit hospitals also routinely utilize monetary incentives in the compensation packages of the C-suite leadership, said Brian B. Sanderson, managing principal of healthcare services at Crowe.

"The compensation structures in the for-profits tend to be much more incentive-based than compensation at not-for-profits," he said. "Senior executive compensation is tied to similar elements as found in other for-profit environments, including stock price and margin on operations."

In contrast to offering generous incentives that reward robust financial performance, for-profits do not hesitate to cut costs in lean times, Escue says.

"The rigor around spending, whether it's capital spending, operating spending, or payroll, is more intense at for-profits. The things that got cut when I worked in the back office of a for-profit were overhead. There was constant pressure to reduce overhead," he says. "Contractors and consultants are let go, at least temporarily. Hiring is frozen, with budgeted openings going unfilled. Any other budgeted, but not committed, spending is frozen."

SCALE

The for-profit hospital sector is highly concentrated. In 2023, there are 5,157 community hospitals in the country, according to the American Hospital Association. Nongovernmental not-for-profit hospitals account for the largest number of facilities at 2,978. There are 1,235 for-profit hospitals, and 944 state and local government hospitals.

On the other hand, the country's for-profit hospital trade association, the Federation of American Hospitals, represents 1,000 tax-paying community hospitals and health systems throughout the U.S., accounting for nearly 20% of U.S. hospitals.

Scale generates several operational benefits at for-profit hospitals.

"Scale is critically important," said Julie Soekoro, former CFO of a Community Health Systems (CHS)-owned hospital. And one benefit of being CHS-owned? The access to resources and expertise, Soekoro said at the time.

Best practices are shared and standardized across all CHS hospitals. "Best practices can have a direct impact on value," Soekoro says. "The infrastructure is there. For-profits are well-positioned for the consolidated healthcare market of the future… You can add a lot of individual hospitals without having to add expertise at the corporate office."

The High Reliability and Safety program at CHS is an example of how standardizing best practices across the health system's hospitals has generated significant performance gains, she says.

Scale also plays a crucial role in one of the most significant advantages of for-profit hospitals relative to their nonprofit counterparts: access to capital.

Ready access to capital gives for-profits the ability to move faster than their nonprofit counterparts, Sanderson says. "They're finding that their access to capital is a linchpin for them. … When a for-profit has better access to capital, it can make decisions rapidly and make investments rapidly. Many not-for-profits don't have that luxury."

COMPETITIVE EDGE

There are valuable lessons for nonprofits to draw from the for-profit business model as the healthcare industry shifts from volume to value.

When healthcare providers negotiate managed care contracts, for-profits have a bargaining advantage over nonprofits, Doran says. "In managed care contracts, for profits look for leverage and nonprofits look for partnership opportunities. The appetite for aggressive negotiations is much more palatable among for-profits."

This article was adapted from previous coverage. Reread it here.

Editor's note: This story was updated on 12/29/2023.

"The growth in healthcare spending in 2022 of 4.1% was more consistent with the pre-pandemic average annual growth rate of 4.4% over 2016-19," Micah Hartman, a statistician in the CMS Office of the Actuary and first author of the report, said in a media release.

"It remains to be seen how future healthcare spending trends will materialize, as trends are expected to be driven more by health-specific factors such as medical-specific price inflation, the utilization and intensity of medical care, and the demographic impacts associated with the continuing enrollment of the baby boomers in Medicare," Hartman said.

Below are a few more key takeaways from the report, and you can read John Commins full report here.

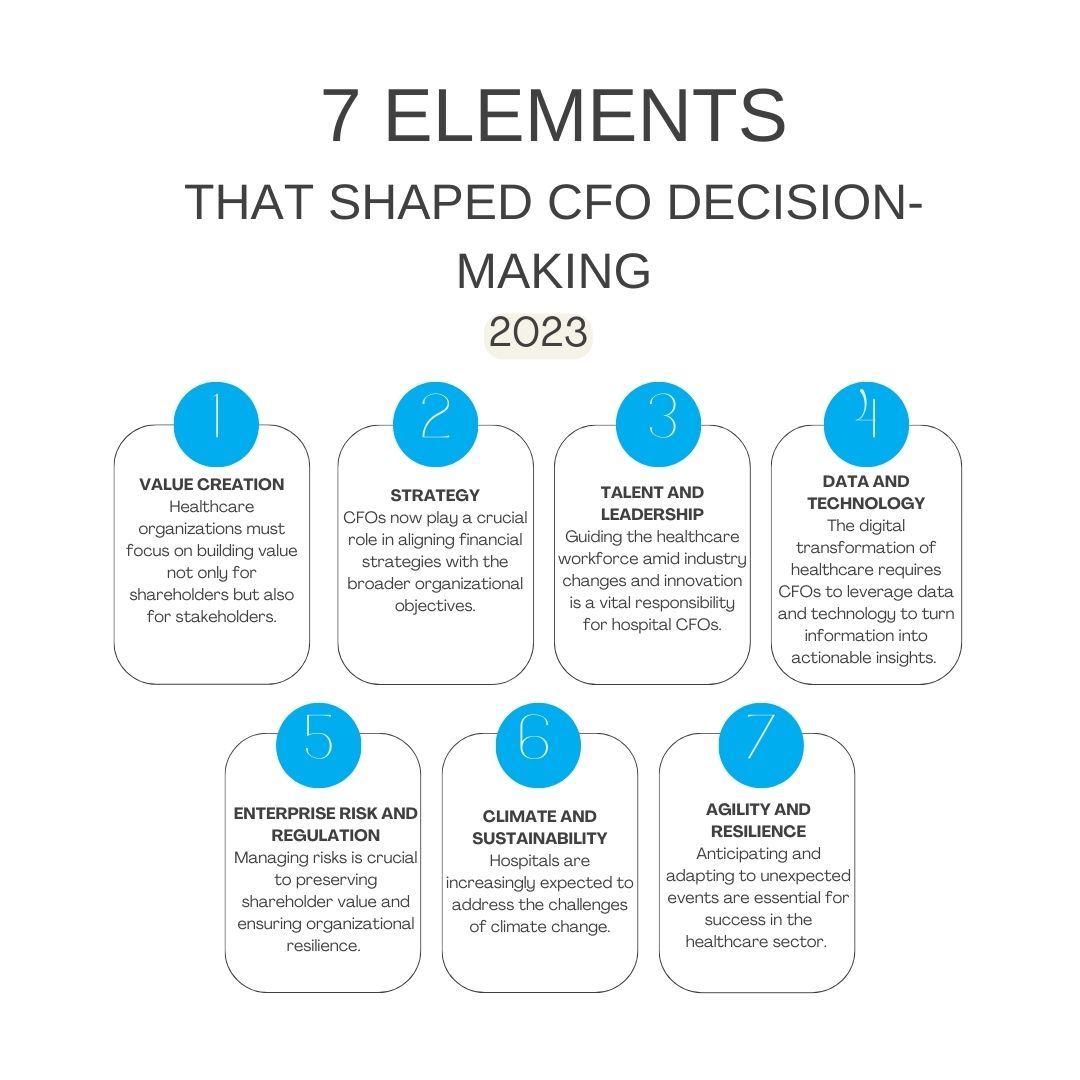

There were seven main threads propelling CFOs' decision making in 2023.

CFOs now find themselves at the intersection of various critical drivers that shape the financial outlook and strategic direction of their healthcare organizations.

So, what were the main threads propelling their decision making in 2023?

There were seven elements that encapsulated the key considerations for CFOs across all industries in 2023, according to Deloitte. Take a look at these seven drivers and read our full story to learn how each applied to CFOs in the healthcare sector.

A new bill may cause a shake-up for hospital and health systems.

The Lower Costs, More Transparency Act, a bipartisan healthcare policy bill, recently passed the House of Representatives, setting the stage for a potential shake-up for healthcare organizations.

This legislation aims to increase hospital price transparency and curb certain practices by pharmacy benefit managers (PBMs).

But why is it significant?

Well, of particular significance is the proposal to equalize payments for drugs in Medicare, whether or not they are administered in hospital outpatient departments or doctor's offices.

Additionally, the bill seeks to postpone payment cuts for hospitals catering to high volumes of uninsured patients until 2026, a delay from the previously anticipated 2023.

Healthcare organizations also need to be on the lookout for increased price transparency scrutiny, especially as many organizations are still struggling with adherence.

What does it mean for CFOs?

Crucial for hospital and health system CFOs is the potential impact of the bill's site-neutral policy on drug reimbursements in Medicare.

Hospitals' opposition to the equalization of drug payments, contending that it would cut into hospital revenue, underscores the financial implications for healthcare institutions

With the legislation projected to reduce hospital payments by over $3.7 billion over a decade, CFOs must carefully navigate the financial landscape amid evolving policies.

The bill also introduces transparency reforms for PBMs, addressing issues of spread pricing and mandating the disclosure of rebates and compensation. This legislative push aligns with broader efforts to scrutinize and regulate PBMs, acknowledging their role in influencing rising drug prices.

For CFOs, adapting strategies to comply with potential transparency requirements and understanding the financial implications of proposed changes will be pivotal.

New data says that health costs have not outpaced the rate of inflation this year, so what can CFOs do?

New data has been unveiled indicating that health costs have not outpaced the rate of inflation this year.

But what does this mean for hospital and health system CFOs? Read on to find out.

The report published by Turquoise Health utilized the list of CMS' 500 shoppable services. To understand the price dynamics of these shoppable services, the report dove into its payer dataset, which contained negotiated rates between payers and providers for all covered services across insurance plans and locations. Payers included UnitedHealthcare, Cigna, Aetna, and Blue Cross Blue Shield.

As of the third quarter's conclusion, there has been a 2% increase in negotiated rates for all 500 shoppable services, aligning closely with the 1.9% U.S. inflation measured by the PCE price index.

Notably, this growth rate remains below the overall U.S. inflation rate determined by the Consumer Price Index. The report highlights specific areas of notable price increases, such as Chickenpox and Measles vaccines, while identifying deflationary trends in services like off-hours medical services, allergy tests, and vaginal deliveries.

For example, in Los Angeles, the negotiated rate for vaginal delivery with post-delivery care varies widely, ranging from $1,183 to $32,563.

What does this mean?

It is crucial for hospital CFOs to recognize that substantial price variations exist for the same care both across different cities and within the same markets, as revealed by the report.

Understanding and addressing these variations is imperative for hospital CFOs to navigate evolving reimbursement landscapes and ensure financial stability.

As the healthcare industry undergoes increased scrutiny on pricing transparency, proactive strategies to manage and standardize costs will be pivotal for financial sustainability.

But where to start? Adoption of the price transparency requirement is key.

It will likely take some time before there is a widescale adoption of that type of pricing feature by providers, but hospitals shouldn't skip steps in the meantime by not doing their part to be as transparent as possible to patients.

"The higher percentage of completeness regarding the publication of machine-readable files and accurate patient estimate tools, the closer we are to empowering patients to gain confidence in knowing how much their healthcare services will cost," Chris Severn, CEO of Turquoise Health, told HealthLeaders.

"Adherence from both hospitals and payers also eliminates a significant burden of negotiating new rates because all rate data will be publicly available, meaning fair rate calculation becomes simpler and accessible," Severn says.

"Overall, these lead to lowering the cost of healthcare."

2024 will be make or break for nonprofit hospitals, says Fitch Ratings.

The outlook is still “deteriorating” for 2024 as staffing shortages and rising inflation is putting the pressure on nonprofit hospitals, according to a recent report from Fitch Ratings.

On top of this, Fitch says downgrades and negative outlooks will likely continue to outpace upgrades and positive outlooks.

Out of these ongoing struggles has emerged a “trifurcation” of credit quality that will only become more prominent in 2024, the report said.

“Much of a hospital’s ability to be successful, will depend on their ability to recruit and retain staff in the currently hyper-competitive landscape for personnel,” said Fitch senior director and sector head Kevin Holloran.

So what does this really mean for CFOs of nonprofits? There are a few key takeaways that CFOs can utilize to remain financially stable in 2024:

Managing salary, wages, and benefits is crucial.

The report highlights that managing the largest single expense for healthcare providers, which is salary, wages, and benefits, is the most important factor for operational success in 2024. CFOs should focus on attracting and retaining staff at all levels to reduce usage and cost per hour of external contract labor, leading to cost savings.

Labor shortages remain a challenge.

The industry continues to struggle with labor shortages, which have been a significant pressure point in recent years. CFOs should anticipate that this shortage will persist in the foreseeable future, potentially impacting operating metrics. Developing strategies to address this challenge and mitigate its effect on operations and financial stability will be crucial.

Incremental operational recovery expected in 2024.

While overall labor supply shortage and financial pressures are expected to continue, the report suggests that there will be incremental operational recovery in 2024. CFOs should plan for this recovery and work towards gradually improving financial performance by addressing key challenges and implementing strategies that align with industry trends.

Some providers may lag behind.

The report also cautions that not all healthcare providers will experience the same level of recovery. Fitch expects a number of providers to lag significantly behind in their operational and financial recovery. CFOs should assess their organization's unique circumstances and actively work to prevent falling behind by prioritizing financial stability and growth initiatives.

Contending with disruptors was top of mind for healthcare CFOs in 2023, and Amazon Clinic gave them a run for their money, literally.

CFOs know that if you choose not to, or simply can’t, partner with the disruptors in your market, be prepared to compete with them.

Market disruptors will be in most markets in no time. Not only are these disruptors targeting the most profitable portions of a healthcare CFO’s business, but they are also more aggressive than the normal competition.

So, who were CFOs seeing as the biggest disruptors in the market in 2023? Look no further than big tech, retail giants, private equity, and national payer vertical integration. This year though, Amazon Clinic was in the spotlight.

Retail giant Amazon is still disrupting healthcare in several ways, but one of the areas Amazon Clinic took aim at this year is somewhere providers are especially vulnerable: price transparency.

As we know, healthcare costs can be incredibly cloudy, so when Amazon Clinic announced its commitment to price transparency, CFOs were forced to rethink their competitiveness in their pricing structures.

Luckily, even though Amazon Clinic represents a major market disruptor for healthcare CFOs, organizations learned that they could adapt and compete by leveraging existing strengths, embracing price transparency technology, and prioritizing the patient experience.

Leveraging Existing Strengths

What Amazon Clinic is attempting to do with their transparent, tiered pricing isn't unheard of and its limitations make it more supplemental than a true replacement of care services, but providers should be getting the message loud and clear that innovation is necessary for them to survive in the future.

Providers still have the homefield advantage as the more trusted source for care and they still have a leg-up by allowing patients to pay with their insurance, a fact that CFOs should leverage.

Embracing Price Transparency Technology

When it comes to price transparency technology, it will likely still take some time before there is a widescale adoption of advanced technology in this space, but hospitals shouldn't skip steps in the meantime by not doing their part to be as transparent as possible for patients.

Streamlining pricing and making it readily available for patients to view is a must, not only in the regulatory space but for bettering the patient experience too.

Prioritizing The Patient Experience

Speaking of patient experience, building greater trust with patients by creating ease of use is a good place to start when a disruptor like Amazon Clinic encroaches an organization’s lane.

"Healthcare, I believe, is still a relationship business and will be at least for a while longer," Kris Kurtz, CFO at University of Michigan Health-West, toldHealthLeaders this year.

"We have patient relationships today for the most part, so it's our business to loosen access, and the ease of use is probably the best strategy we can deploy. As an industry, we make it far too difficult for patients to enter and navigate the system. In some instances, we may need to partner with the disruptors rather than compete with them. [Likely it's] probably a combination of both," Kurtz said.

CommonSpirit Health's latest earnings report was a mixed bag, but ultimately the system was left with a large operating loss.

CommonSpirit recently released its fiscal year 2024 first-quarter results, which ended September 30, where gains were largely offset by costs.

The health system experienced robust volume growth, reflected in increased adjusted admissions and outpatient and ED visits, the report showed. However, these gains were offset by rising costs, particularly elevated labor costs and inflation rates surpassing payer reimbursement rates.

The financials, with operating revenues at $8.87 billion and operating expenses at $9.16 billion, resulted in an operating loss of $291 million and EBITDA of $237 million, with margins of -3.3% and 2.7%, respectively.

Despite these challenges, the health system remains proactive, implementing initiatives to enhance efficiency and financial stability in supply chain, pharmacy, payer contracting, and purchased services, the report said.

The commitment to market-based growth strategies, including the development of ambulatory offerings and integrated delivery networks, underscores CommonSpirit's resilience amid industry headwinds.

But will it be enough for CommonSpirit to see some black next quarter?

Time will tell, but between consistent losses and layoffs, the system may need to fight its poor margins for a bit longer. In fact, CommonSpirit reported a $1.4 billion operating loss and a $259 million net loss for its 2023 fiscal year, which ended June 30.

In the video interview excerpt below, Tande discusses how this new bill with impact the payer/provider relationship and how Scripps plans to help “bend that cost curve a little bit more.”

0c75.jpg?itok=nIbFQSVj)