The attack is rippling through the healthcare industry and affecting everyone, including payers.

News of the Change Healthcare ransomware attack is plastered everywhere.

Late last month the technology company that was purchased by UnitedHealth Group, saw a massive cyberattack that is still being felt by health systems across the country.

As we know, Change Healthcare, a company that processes medical payments, touches about one out of every three patients in the U.S. One of the main challenges from this attack has been for providers as they are struggling to access the data they need to process prior authorizations and claims in order to get paid.

It also had a great effect on pharmacies, hospitals and patients trying to access their prescriptions. Patients and their insurance coverage are also feeling the effects, with many consumers paying out-of-pocket to get their refills.

The attack has, overall, wreaked havoc, with some health care providers losing up to an estimated $100 million a day.

On March 5, HHS stated that it would expedite payments to affected hospitals and get other workarounds in motion. CMS is also stepping in, encouraging Medicare Advantage systems and Part D sponsors to relax or remove prior authorizations. It’s also asking MA plans to offer advanced funds to providers and encouraging providers to ask for new electronic data interchanges from their MA contractors to process claims, and to inform their contractors that they must accept these manually processed claims.

So far, Change Healthcare has been hit with six class-action lawsuits following the attack, including three in Tennessee and two in Minnesota where parent company UnitedHealthGroup is headquartered.

On March 12, AHIP released a statement response to the attack, saying:

“Given the very wide variability of impact across the system, individual plans and providers are in the best position to assess how to maintain appropriate payments in a timely manner—and also to minimize the need for reconciliation processes.”

The response goes on to note that exemptions from prior authorizations during this time when systems are making advance payments could expose patients and employers to “fraud, waste and, unnecessary costs.”

The American Medical Association was not impressed with AHIPA’s seemingly lackadaisical response; President Jesse M. Ehrenfeld MD, MPH called out the response as a dumbfounding “business as usual approach” after weeks of silence and lack of assistance by AHIPA.

“This approach is particularly galling since service outages have exacerbated the administrative burdens and care delays already associated with this process,” said Ehrenfeld. “Prioritizing profits over the stability and solvency of our care delivery system starkly contrasts with the Biden Administration’s appeal to health plans to “meet the moment.”

The Effect on Payers

As The Biden Administration and HHS dial up the pressure on payers to create a bridge by making advanced payments to providers, some are feeling the effects of the attack more than others.

Aetna sent a message to providers stating that it is aware that some of its providers are experiencing the lack of timely payments. The insurer said it is working to assess the impact on claims payments and recommended its providers to use other approved transaction vendors. Aetna said it would not “liberalize any prior authorization requirements at this time.”

Humana uses Change Healthcare’s system for about 20 percent of its provider claims before it reaches the insurer, thus making it difficult to examine the total medical expenses, reported Bloomberg. Humana also uses Change for their dental and D-SNP business and said it is still evaluating the effects of the hack. Humana, as well as Elevance have already moved to Change competitor Availity to process payments.

As for UnitedHealth, the insurer has announced two programs to advance funding to providers and has encouraged its rivals to do the same.

Insurance reps are on track to meet with U.S. health officials, reported Bloomberg. This meeting follows an earlier meeting this week attended by UnitedHealth Chief Executive Officer Andrew Witty, along with other industry executives and top US health officials.

The Aftereffect

As we see scrambling providers and frustrated payers, this event may even impact payer-provider relations down the road. How a payer handles this situation and whether or not they make these timely advanced payments to their provider may set the tone for future contracts.

When it’s time to renew contracts, will providers wave off their payers who didn’t provide timely payments or assistance during this crisis? It’s too soon to tell, but one thing is sure: the interdependence of the healthcare industry is vital, especially in times like these.

The 2024 HIMSS conference sparked several innovative discussions amongst leaders.

Tech solutions are taking off, and the 2024 HIMSS conference brought about many important conversations surrounding some of the industries biggest pain points. From ethical AI use to efficiently streamlining data, check out the main talking points.

AI is Taking Off. No longer grounded to the conception stage, AI is moving up to actual implementation and industry benefits. HIMSS24 brought about numerous AI announcements as vendors unveiled use cases and ROI examples.

As new AI centered partnerships spring up, providers are collaborating with EHR designers and digital health companies to streamline data for doctors and nurses to improve care and ultimately, their work-life balance. One popular case that tech leaders are zooming in on is that of ambient AI which has the ability to capture conversations and turn them into clinical notes, which could, in time, take the tedious process of note taking out clinicians hands.

AI Value and Governance. Already a familiar conversation, the governance of AI has turned everyone's head. Financial value vs clinical outcomes was a big conversation as the Coalition for Health AI (CHAI) released its newest collaborations aimed at creating guidelines for the ethical use of AI.

Conversations about the ethical use of AI have popped up everywhere with looming questions around value, AI use by payers in claims management, and government guidance.

Cyberattacks. Cybersecurity is obviously still a massive concern. As health systems continue to flounder in the recent cyber attack on Change Healthcare, which even limited attendance this year at HIMSS, industry leaders are focused on how their organizations can limit damage when the next inevitable cyber attack hits.

The Foundation of Data. HIMSS24 kept its longtime focus on interoperability. The innovation conversation is shifting from “how can these new gadgets help?” to “how can we gather, store and manage data better?” Connectivity seems to be the overarching solution, as health leaders examine solutions that create digital data highways from patient to care team.

Providers are looking at strategies and tech can help them take in, sort and efficiently use the data they want and need. To handle these massive amounts of data, providers will be looking at solutions that are fast and limit their manual labor, regardless of EHR platform and HIT framework.

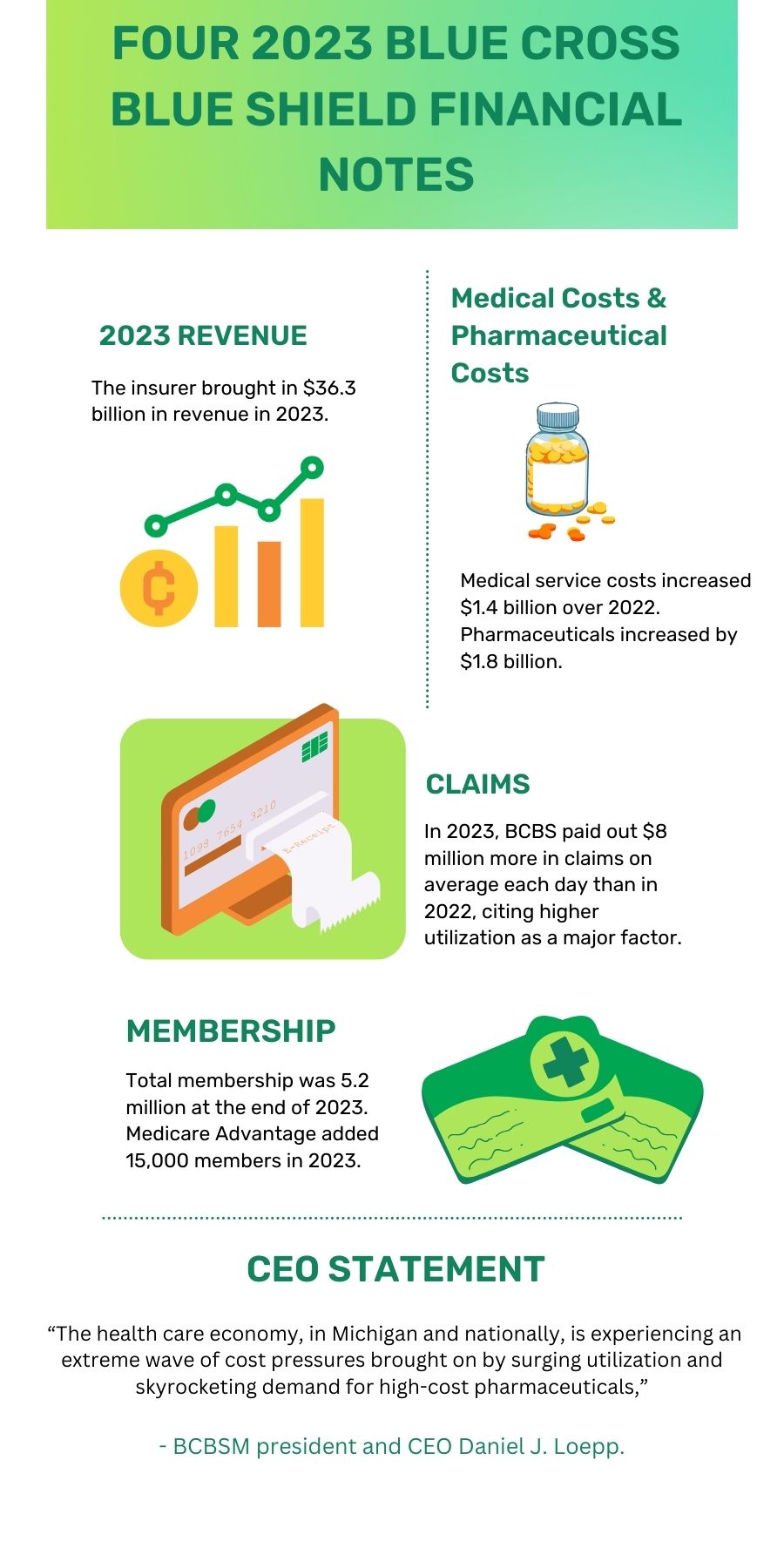

A new release showed the Detroit-based insurer had a net income of $100 million in 2023, which was 0.2% of the insurer’s total revenue. This was up from a $777 million loss in 2022.

Driven by increased medical costs, the company reported a $544 million underwriting loss, but it was later offset by earnings in investments and subsidiary profits.

In the news release BCBSM CEO stated: “The health care economy, in Michigan and nationally, is experiencing an extreme wave of cost pressures brought on by surging utilization and skyrocketing demand for high-cost pharmaceuticals,” said BCBSM president and CEO Daniel J. Loepp. “Despite these extraordinary pressures, Blue Cross retained our membership, managed a positive financial margin, and continued our dedicated efforts to promote affordable health coverage for our members in 2023.”

A handful of specific items affected BCBS’s finances in 2023. Other payers can note the uptick in pharmaceutical expenses and how Medicare Advantage kept BCBS’s total membership strong.

Check out the infographic below to see four items to note about BCBS’s 2023 finances.

The new ratings come after the insurer sued the federal government in January.

Elevance Health will now have four Medicare Advantage (MA) contracts with higher 2024 ratings after CMS updated the original scores announced in October, according to a regulatory filing.

According to the filing, Elevance estimates that about 49% of its MA members will be enrolled in a plan with at least four stars in 2024. As a result, Elevance will see approximately a $190M payout for 2025.

Following the pandemic, CMS made stricter adjustments to how it issues MA star ratings. When the original ratings were announced in October, Elevance members that were enrolled in plans rated at four stars or more dropped from 64% in 2023 to 34% in 2024.

Three of the insurer’s biggest MA contracts (based on enrollment) dropped from 4.5/4 stars to 3.5 stars. The ultimate impact of the lower ratings meant a $500 million drop in Elevance’s revenue for 2025.

What happened?

Elevance sued HHS back in January over alleged miscalculations in their MA star ratings. The insurer was set to lose $190Mㅡthe same amount it will gain after the revised ratingsㅡafter its call center missed a single call from CMS. CMS denied giving the insurer five stars on this measurement because it did not meet the 99% success rate, but Elevance states that the call dropped through no fault of its own.

The lawsuit also argues that it would have been impossible for Elevance to meet that success rate, as CMS used a calculation method that mathematically wouldn’t have allowed the cut point to be reached unless not a single call was missed.

During the pandemic, relief provisions caused Medicare star ratings to inflate. Regulators saw this inflation and took steps to reel in ratings, resulting in less plans achieving the four-star threshold. Payers bonuses therefore suffered in 2024, falling to 42% compared to 51% in 2023.

While CMS cannot increase or decrease cut points by more than 5% each year, it calculates cut points for specific individual measures to determine a plan’s score on that specific measure.

In 2020 CMS finalized its usage of the Tukey method to decide 2024 star ratings; this involved removing outlier contract scores to avoid influencing cut points. This made it more difficult for plans to earn high ratings because most outliers are on the lower end and removing them shifted cut points to a higher range.

In the lawsuit Elevance argued that the Tukey method was used as an "unlawful, and arbitrary and capricious" methodology to change star ratings. The insurer argued that Tukey does not consider the 5 percent guardrail for cut points and therefore CMS violated the guardrail regulation when deciding 2024 star ratings.

What does it mean for other payers?

Elevance was able to sue HHS and garner new, improved ratings, but could other insurers follow with the same argument?

As Elevance basks in its newfound star ratings, other insurers could look at its legal action against HHS as a guide for how to argue for better ratings.

Oral arguments for the case were heard on Monday, and payers need to pay attention.

Hundreds of millions of Americans depend on the no-cost sharing coverage of preventative services by the ACA. Now that coverage is being threatened as the Braidwood case moves forward in the court.

As we know, in September 2022 a lower district court ruled that Braidwood Management, a Christian-owned nonprofit, should not be required to purchase insurance plans that cover PrEP drugs for HIV, claiming it violates their rights under the Religious Freedom Restoration Act. The lower court ruling was appealed by the federal government in March 2023 before it went into effect.

On Monday the Fifth Circuit Court of Appeals listened to oral arguments for the case to decide if the appeal by the federal government was unconstitutional.

Preventative services are a vital part of the ACA and without this coverage millions of Americans would lose a critical part of their healthcare—sending a ripple effect through the insurance industry and could mean big changes for payers.

The final decision will come in a few months, but regardless of the outcome, this ongoing case will most likely get appealed up to the Supreme Court.

What Happened In Court

The hearing held on March 4 presented an argument in deciding if the entities involved, particularly the U.S. PSTF, were unlawfully appointed. It was argued that the PSTF violates the appointments clause because this entity was not appointed by the president, a court or senior department head.

It was also argued that all entities violated the nondelegation doctrine, which would forbid Congress from delegating responsibilities to administrative agencies under certain cases. The district court ruled the ACA did not violate the nondelegation doctrine, but it did leave open the possibility a higher court could disagree.

Starting off, Judge Southwick inquired how the PSTF could correct its own unconstitutional authority. In order for individuals to have the protection the ACA preventive services offer, the whole market would have to adjust.

Judge Southwick said he wasn’t sure what relief would be appropriate. “[...] but it does seem to me that that does undermine everything they did,” he said.

Alisa Beth Klein, arguing on behalf of the Department of Justice, emphasized the fact that with this case, timing is everything; the whole point of the preventative services that Congress said must be covered without cost sharing is for individuals to have them in a timely fashion, so they don't get a disease at a point where the survival rates are much lower. It was also mentioned that the district court does not have to vacate universally, and they could consider a more limited remedy, injunctive, declaratory, or otherwise.

Jonathan Mitchell, representing Braidwood Management argued: “The government's request for a partial stay of the district Court's judgment pending appeal should be denied for numerous reasons. [...] there is no evidence or reason to believe that any private insurer or employer will drop or limit coverage of statutorily required preventive care in response to the district Court's ruling.”

Judge Southwick dismissed Mitchell’s argument here as speculation, saying it asked them to predict how insurance companies would react.

“How emphatic does your state of desire or your state of intention need to be to buy this particular product?” Mitchell asked, inquiring if the absence of a particular choice among products is enough to be considered injury.

Moving on in the case, Mitchell shifted the focus from Braidwood—that has its own self-insured plan and got the relief it wanted at the state level—to other Texas plans, where research showed they offered the preventative services prior to the ACA mandate.

In order to balance the equities, these individual claims must be examined.

Mitchell went on to explain that the appeals court decision that reverses the District Court could drop at any time in the middle of a planned coverage year.

“[...] if there is a statutory departure or a violation taken by any person, private insurer or private employer in reliance on this judgment, they could be hit with penalties under the ACA, even if they acted in reliance on a District Court injunction that later gets vacated,” Mitchell said.

Overall, the case seeked to challenge the legality of the entities involved and how to solve any damage or confusion they might have caused, as well as how to give standing to the individual plaintiffs and separate them from the Braidwood case.

By the end of the hearing Klein reminded the court what is at risk: “It can't be overstated how important this guarantee of cost-free access is for the 150 million people who aren't here to protect themselves, who can otherwise be assured that when they go to get their mammograms or statins or colonoscopies or lung cancer screening, etcetera, that there's no out of pocket cost.”

What It Means For Payers And What Could Be Next?

While this case may not seem like it directly correlates with payers and their operational or financial endeavors, they should pay attention.

Preventative services by the ACA help hundreds of millions of Americans fight illnesses, and without these services, population health could be at a major risk. The effects of preventative care are not seen until years down the road, so there’s no instant economic value to payers, but they must look ahead to analyze the effect this could have on their members and the threat it could pose to their future costs and utilization.

Depending on the outcome of his case, it could possibly send insurance beneficiaries shuffling down the line to find coverage for these services. This coverage will most likely still be sought out elsewhere by beneficiaries.

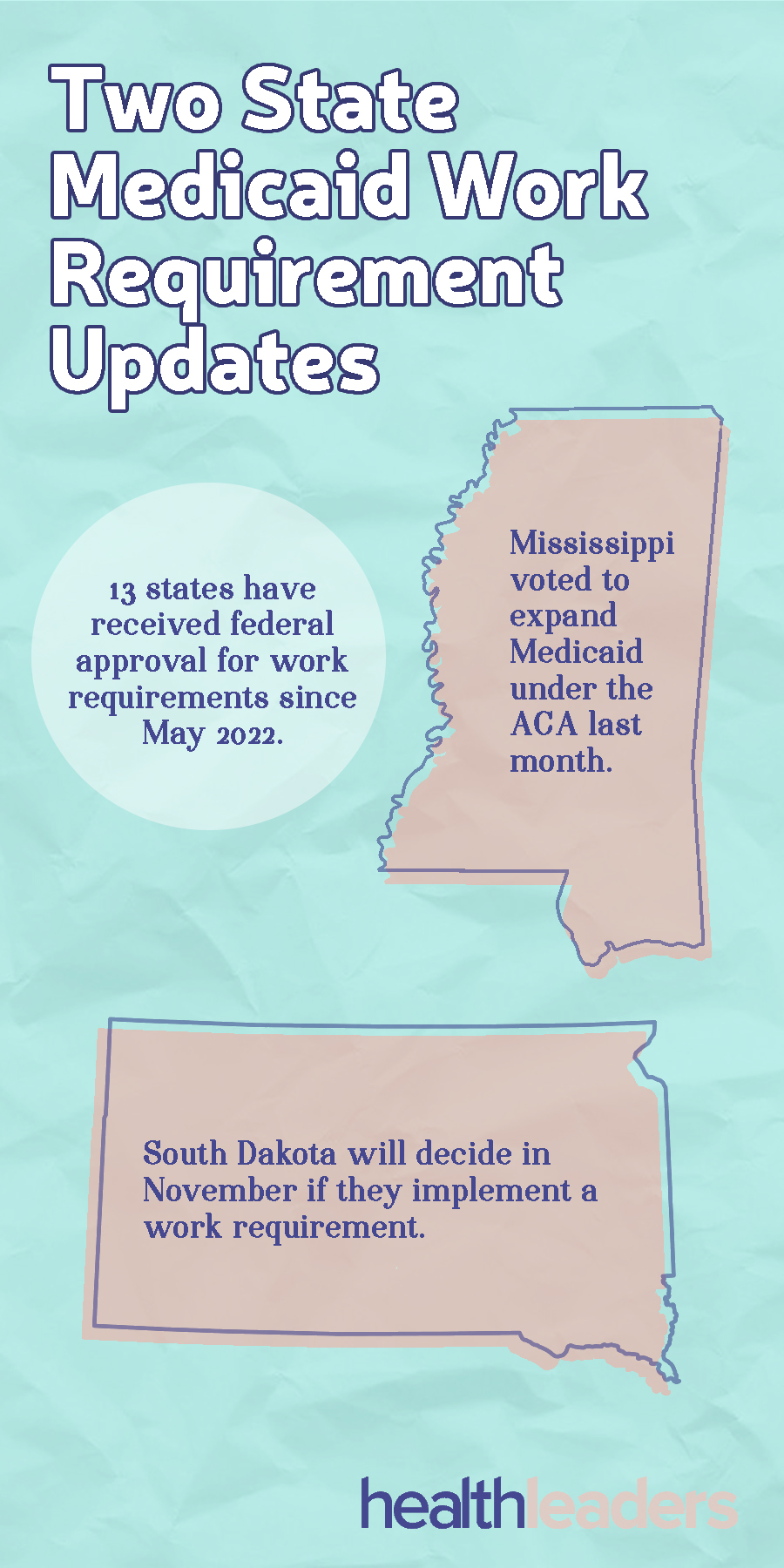

Will new Medicaid expansions be followed by work requirements?

More and more states are expanding Medicaid and work requirements are following. Recently, two more states have added work requirements for Medicaid coverage.

Mississippi

Mississippi voted to expand Medicaid under the ACA last month and the new expansion issues a work requirement, but the Biden Administration could refuse to allow the state to implement it.

Gov. Tate Reeves has notoriously opposed Medicaid expansion, often derisively referring to it as “Obamacare expansion.” Reeves will most likely veto the bill but a report stated that the legislature could override his veto with a two-thirds vote from both chambers.

South Dakota

Coming this November election South Dakota voters will decide if they may implement a work requirement for Medicaid. The issue has been approved by the state House and Senate, but will still require approval by the Federal government in November.

The expansion took effect last summer. According to a report from AP News Republican Rep. Tony Venhuizen, who spearheaded the issue, said during a panel, “If this amendment was approved, and if the federal government allowed a work requirement, and if we decided we wanted to implement a work requirement, two or three steps down the line from now, we would have to talk about what exemptions are available.”

Cigna and Trinity Health sign off on multiyear deal after months of negotiations and a disruption of coverage.

Cigna and Trinity Health of New England have struck a multiyear deal after months of contentious negotiations that left patients out of network.

Cigna’s original contract with Trinity that covered Mount Sinai Rehabilitation Hospital, St. Francis Hospital, and Trinity Health of New England Medical Group providers in Connecticut expired on January 1.

The new deal, which started March 1, applies to those facilities as well as St. Mary’s Hospital in Waterbury and Johnson Memorial Hospital in Stafford, which have agreements that do not expire until April 30, according to a report from the Harvard Business Journal.

While full details of the agreement were not released, this new deal will extend coverage to all of Trinity Health’s facilities in Connecticut.

Why It Matters

Payer and provider negotiations have become more contentious as providers face rising health costs. Providers are pushing back against payers to cover these costs as payers are feeling the pressure to curtail premiums.

And, as in this case, this can mean a disruption in coverage for patients while the two parties work on an agreement.

“We worked diligently to negotiate an agreement that covers the true cost of the care we provide—which is critical to ensuring our Regional Health Ministry can continue to invest in the medical staff, care innovations, and health programs our community expects and deserves, because Health Comes First,” Trinity said in an announcement.

“While we wish this agreement could have come without going out of network with Cigna, we look forward to continuing our partnership.”

Trinity’s announcement addressed the two-month-long disruption of coverage for their patients and encouraged them to contact the number on the back of their Cigna insurance card to ensure they will be covered at in-network rates as they resume scheduling appointments.

As more payers and providers continue to battle, we may see more providers going out of network temporarily, or permanently, as a way to even the playing field.

Trinity’s Push For More Data

In January Trinity Health also struck a multiyear deal with Anthem Blue Cross Blue Shield of Connecticut. This agreement mentions that the two would collaborate on several initiatives “including advanced data connectivity and value-based care models designed to improve health outcomes and better control costs for Trinity Health patients covered by Anthem health plans.”

The announcement on Trinity’s website stated that the two organizations will incorporate the Epic Payer Platform into regular operations that will work to streamline patient data flow, among several other operational efficiency goals.

“Our shared focus on simplifying the healthcare ecosystem, removing barriers to care, and overcoming administrative hurdles for doctors and clinicians is a particularly rewarding aspect of our relationship with Trinity Health,” said Anthem Vice President of Networks Jordan Vidor.

Trinity Health’s newest deal with Cigna did not include collaborative goals such as these. Harvard Business Journal reported that Kaitlin Rocheleau, a spokeswoman for Trinity Health, said the new agreement with Cigna "does not yet include collaboration on data connectivity and value-based care models, but we intend to continue those discussions."

Healthcare C-suite execs flocked to ViVE this week in Los Angeles.

The 2024 ViVE conference in Los Angeles is sparking innovative conversations. AI and cybersecurity were among some of the big topics, and health leaders are looking for more action and ROI in these spaces. Nursing was also top of mind, with healthcare executives talking about how they can improve workflows, reduce stress, and boost patient care

The recent proposed MA rate cuts could cut into payers’ profits, and payers are fighting back.

Medicare Advantage (MA) has long been a favorite of payers, often doubling their profits. But will potential rate cuts send payers fleeing out of the program?

Originally, CMS expected MA rate cuts to drop about 0.16%. But a recent study from the payer lobbying group Better Medicine Alliance, which represents payers in Medicare, found that if the proposed rates are approved, next year MA cuts could drop by 1% per month per beneficiary.

Payers are arguing that CMS didn’t consider higher utilization, which has increased considerably among seniors.

So where did the CMS go wrong?

The Growth Factor

Insurers are saying CMS failed to take the growth factor—and how the growth rate is affecting payers’ spending—into consideration when calculating the proposed rates.

With increased costs at play, the growth factor is vital in calculating the overall MA reimbursement rate. For 2025, regulators calculated a growth factor of 2.4%, but realistically, it’s leaning more towards 4-6%, according to the Berkeley Research Group analysis.

This change is likely to affect premiums and supplemental benefits for members. Since the second quarter of last year, MA saw an uptick in care utilization, especially in outpatient care such as hip and knee surgeries/replacements. With this trend continuing, payers are seeing a dip in their profits from premiums.

The Lobbing Effort

Now, payers are urging regulators and administration officials to pressure CMS to change the proposed cuts before the finalization goes through on April 1.

Although this may not spur the lobbying efforts we saw by payers last year, it will however still most likely include a digital ad strategy to oppose the newest cuts. American seniors have already taken to organizing meetings on Capitol Hill to protest the changes, saying that they don’t want their coverage to change.

The Earnings Outlook

For payers who lean hard into the MA market, the proposed cuts could ruffle some feathers.

Humana, which brings in a large portion of its revenue from Medicare, brought forward an internal analysis that said the cuts would cause its funding to drop by 1.6%. Cetene (also a MA-heavy insurer) complained the cuts would drop its rates by 1.3%.

The cuts will certainly have effects, but probably not as intensely as payers are anticipating. The fact is that only two insurers, CVS Health and Humana, are actually looking at a cut in their 2024 earnings outlook coming into this fiscal year, citing higher medical costs.

But these cuts are not exactly spelling doom for payers in the MA market, CMS says.

CMS stated that from 2024 to 2025 MA payments from the government to MA plans are expected to increase on average by 3.7%, or over $16 billion.

MA may not be the cash cow for payers that it used to be. Although the proposed rates will likely be lowered, payers are still likely to intensify their coding practices, up premiums, and drop some benefits, hurting beneficiaries who are comfortable in their current plan.

If it stands, the final rule could send payers exiting what they consider an underperforming market.

Will the dip in profits cause some payers to jump the MA ship altogether?

Comments on the matter are due March 1, so we’ll check back in April.

Employers are seeking claims data, but payers are refusing.

Employers are at odds with payers over their cost and claims data.

Claiming that insurers consistently block access to this data, employers are saying it is increasingly difficult or even impossible to understand what they are being charged in their health plans. Despite a federal mandate that restricts health plans from limiting access to this valuable data, employers are still struggling to obtain it from insurers, turning to lawsuits as a last resort.

In 2021 The Consolidated Appropriations Act (H.R. 133) required employer sponsored health plans and health insurance companies to affirm by the end of 2023 that their contracts don’t contain “gag clauses” that would restrict the handover of information about the cost or quality of medical services.

But it hasn’t been that simple.

What’s happening?

As employers begin to use hospital and health plan data to compare prices and create well-structured plans, some questions are rising, and payers aren’t answering. Much of the time, employers and plan sponsors say that insurers are refusing to hand over their claims data, leading to federal investigations.

This dynamic has led to a push from Congress and some states to stiffen the legal requirements to ensure health plans have access to their cost and claims data.

The argument employers, and specifically member benefits directors, are making is that their plans need to access their claims data to check that payments made to medical providers are accurate, which can sometimes far exceed the actual billed amounts.

Some insurers are arguing that they do provide information about their plans, but only when specifically authorized by the state.

According to an article by Bloomberg, Health Care Service Corporation (HCSC) discussed the possibility of allowing a data warehouse to provide the information to employers, but that would be accompanied by a whopping $20,000 price tag. That’s not the answer employers are looking for.

In June of last year Kraft Heinz filed a complaint that Aetna “breached its fiduciary duties and engaged in prohibited transactions” through permitting undisclosed fees and processing medical and dental claims without human review. Aetna never commented on the complaint, and the matter was moved to arbitration.

Do unresolved complaints turn into lawsuits?

In December, labor unions that were contracted with Elevance Health sued the insurer, claiming the giant did not allow employers access to their own claims data and then charged the plans higher rates than what it negotiated with hospitals.

Employers are fed up with paying the higher fees. Studies show that when employers do have access to this data, they are able to significantly reduce their costs.

What does this mean for hospital and health system leaders?

And as we know in healthcare, reducing those benefit costs are important to hospital and health system leaders. As labor costs in general are weighing heavy on CFOs, they are now playing a bigger role in healthcare benefit decisions.

The breadth of information they consider in making health plan design and purchasing decisions has expanded well beyond monthly premiums and cost sharing, and claims data access could play an important part in that decision making.

In fact, a study by NIH that examined employers' access to claims data stated: “Employee health claims data offer a unique opportunity for employers to yield additional savings in the long run through implementation of wellness and other targeted programs and have a lasting, positive impact on their employees.”

As the struggle continues, the payer landscape could see more lawsuits like the Kraft/Aetna case in the future; and maybe even with a hospital or health system. Will the action and complaints from employers be enough to get insurers to loosen their grip on their data?

titlea788.jpg?itok=taGsemcC)

.jpg)

.jpg)