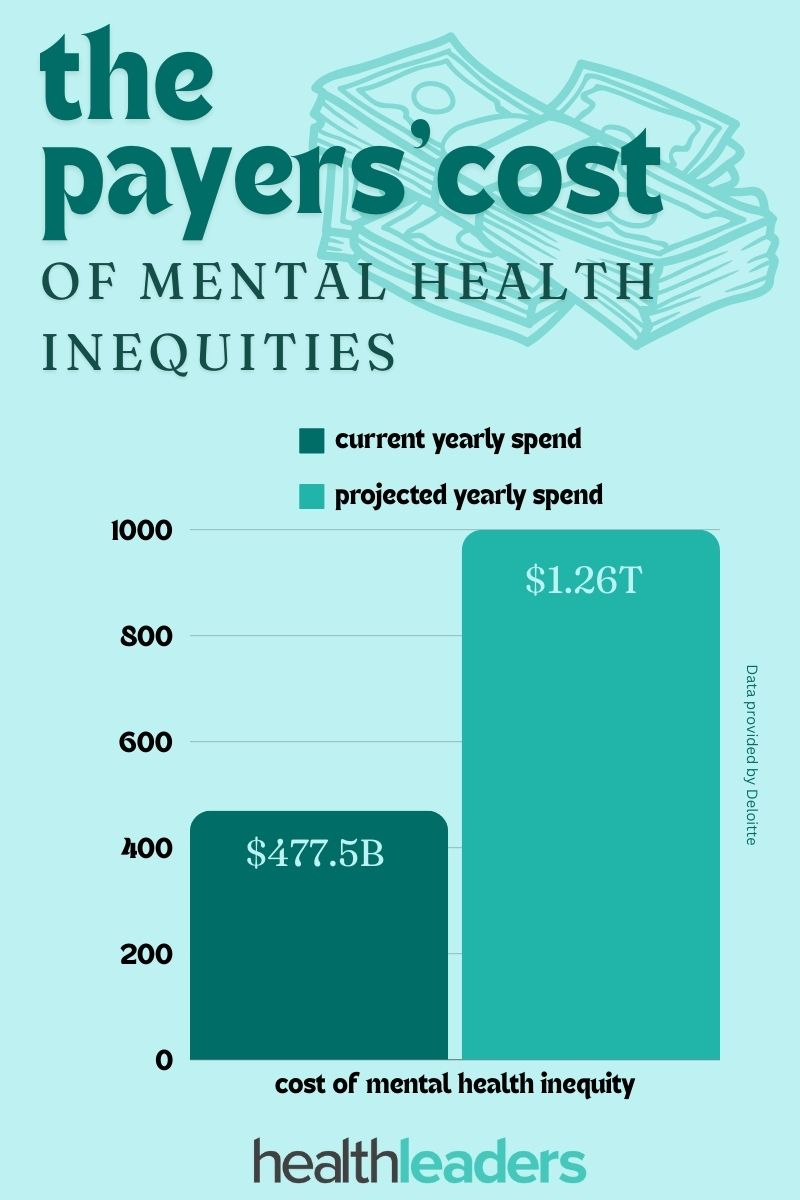

Unorganized mental health care is driving up utilization costs.

The inequities of mental health care are costly and prevalent throughout the nation. If left unaddressed, the U.S. will may spend almost half a trillion dollars in unnecessary costs for mental health care through 2024. That number could even escalate to $14 trillion by 2040 if left uncontrolled, according to a report from Deloitte and the Meharry School of Global Health.

According to the report, the U.S. currently spends about $477.5 billion annually in avoidable expenses related to mental health inequities. Year by year, the U.S. is expected to spend roughly $1.26 trillion on these inequities.

The report also shows that emergency department utilization, in relation to mental health inequities, costs the healthcare system about $5.3 billion annually. Projections suggest this may rise to $17.5 billion by 2040, if left unaddressed.

The problem is that many individuals don’t have access to quality mental health care, particularly communities that are already underserved. Roughly 57% of these groups don’t have access to care, according to the report.

This issue affects the health system as a whole, but payers in particular stand to face soaring utilization costs. If payers can shift their focus to mental health care management, they can implement care strategies that can make a big difference. If the groups facing these inequities acquire access to preventive mental health services, issues can be addressed early on and reduce emergency department visits.

Payers can help in closing this care gap by implementing innovative mental health care strategies through their care management platforms. If these issues are addressed the report suggests it could lead to a notable decrease in not only ER visits, but also a decrease in premature death and productivity loss due to cardiovascular disease, plus all the costs associated with its management.

Unorganized mental health care is driving up utilization costs.

The inequities of mental health care are costly and prevalent throughout the nation. If left unaddressed, the U.S. will may spend almost half a trillion dollars in unnecessary costs for mental health care through 2024. That number could even escalate to $14 trillion by 2040 if left uncontrolled, according to a report from Deloitte and the Meharry School of Global Health.

According to the report, the U.S. currently spends about $477.5 billion annually in avoidable expenses related to mental health inequities. Year by year, the U.S. is expected to spend roughly $1.26 trillion on these inequities.

The report also shows that emergency department utilization, in relation to mental health inequities, costs the healthcare system about $5.3 billion annually. Projections suggest this may rise to $17.5 billion by 2040, if left unaddressed.

The problem is that many individuals don’t have access to quality mental health care, particularly communities that are already underserved. Roughly 57% of these groups don’t have access to care, according to the report.

This issue affects the health system as a whole, but payers in particular stand to face soaring utilization costs. If payers can shift their focus to mental health care management, they can implement care strategies that can make a big difference. If the groups facing these inequities acquire access to preventive mental health services, issues can be addressed early on and reduce emergency department visits.

Payers can help in closing this care gap by implementing innovative mental health care strategies through their care management platforms. If these issues are addressed the report suggests it could lead to a notable decrease in not only ER visits, but also a decrease in premature death and productivity loss due to cardiovascular disease, plus all the costs associated with its management.

A big problem for payers will call for big solutions.

Editor’s note: Part one of this two-part article discussed the impacts that climate change will have on healthcare, and the role payers will need to step into to address climate change and protect their businesses. Part two looks at more detailed solutions that payers can implement so their business doesn’t get washed away.

Climate change is bound to majorly impact every health plan on the planet, but payers don’t have to be left stranded. Getting an early start on climate change planning before it gravely threatens health plans is the best option for insurance businesses to not be left high and dry.

“The climate crisis is a health care crisis,” says Baylis Beard, director of sustainability for Blue Shield of California., “As insurers, we are part of the healthcare industry, which means we have a responsibility to decrease our emissions and use our voice to lead the way to a more sustainable, healthier future.”

Climate change will impact payers in three key ways: high utilization, high costs, and weather-related events that will affect healthcare workers.

High Utilization

Creating a Plan

Payers should develop climate change response plans to focus on their high-risk areas, the areas that will eventually cost them the most to cover. That might include implementing digital care and telehealth solutions. Payers can create ways for consumers to educate themselves about high-risk areas, possible health effects, precautions to take, and resources available to them if they are located in a high-risk area. By leveraging care-management platforms, payers can provide information like inclement weather alerts and educational content to allow their members to stay informed in an accessible way.

Keeping track of member health will play a greater role as climate change advances, particularly with seniors and the Medicare Advantage population. Studies show that seniors in particular will be greatly affected: “Among other alarming facts, heat-related mortality for people above age 65 has increased by more than 50% in just the past 20 years,” according to a report from the Patient Safety Network.

Research

High-risk areas might not always be easily identifiable, and this may take some research to create an accurate response plan.

For example, California experiences frequent wildfires, and long-term exposure to smoke inhalation kills thousands each year. However, according to one study , only about 1,700 of the 6,300 deaths that occurred each year from smoke inhalation between 2006 to 2018 occurred in the West. This study shows that wildfire smoke had the most prevalent effects in the East because of how fast the smoke traveled. The point: don’t make assumptions without looking at all the data.

“Much of the research on the effects of climate change on health has been done with clinical data to understand health outcomes,” said Blue Shield of California’s director of sustainability Baylis Beard, “but the impact on healthcare utilization and costs is less understood.”

In order to uncover the true cost of climate change for health insurance, payers should focus on using science and evidence-based strategies. An article by the Patient Safety Network states: “Evidence-based strategies are required to accelerate healthcare decarbonization and avert the worst predicted harms to health and healthcare systems.”

Further, insurers can collaborate with climate change researchers and weather institutions to create comprehensive plans that take into account a vast array of climate data.This avenue can ensure the most accurate results can be reflected when payers analyze the financial impacts.

High Costs

Perhaps the biggest and most obvious effect of climate change will be higher costs. High utilization leads to high costs for payers, but what will also step into the spotlight? Supply chain malfunctions.

The United States’ healthcare sector emits about a quarter of total global healthcare emissions. In other words, the U.S. healthcare industry uses a lot of energy, and transports a lot of supplies. Climate change will bring about disasters that are very difficult to prepare for in this sector.

For example, a tornado that ripped through a Pfizer drug warehouse in North Carolina in July of 2023 destroyed medications as well as pharmaceutical raw materials, exacerbating the shortage of drugs used in surgery and cancer treatment.

Payers can work with outside organizations to create communication plans on how they will handle these events. But they must make sure the select the right partners. “We play a role in creating the right incentives in the value chain and choosing sustainable partners,” said Beard.

Climate Change Affecting Healthcare Workers

The biggest issue in healthcare is the labor shortage. Climate change will worsen this. Extreme heat and weather will affect certain occupations more than others.

For example, studies show that climate change will have a big effect on emergency response workers. The Journal of Emergency Medical Services published an article stating: “Prolonged heat waves strain EMS staff and resources, emphasizing the need for strategic planning and collaboration with other agencies.”

Payers should collaborate with their health systems to ensure there are resources for these workers when they feel strained. Along with EMS workers, doctors and nurses facing intense burnout from high volumes of patients after weather-related events will also increase. Implementing AI and automation to cover tedious tasks and mitigate stress is one tactic that can help.

Virtual Care

Virtual care is going to play an even bigger role as the climate crisis worsens. The healthcare industry has already gotten a jumpstart on this type of care because of the COVID-19 pandemic. Telehealth and virtual care have been shown to decrease emissions as well as water use. While virtual care can have its limitations, including broadband issues and limited access to technology, it can provide care when physical access to a health system is just not possible. Payers should look at updating their virtual care models and implementing new forms of virtual care. For example, Blue Shield of California has implemented a new virtual care platform that connects members with virtual primary care services for patients to access providers via mobile phone, tablet, or personal computer.

“This virtual care platform also helped provide critical health care services to a town badly damaged by the Camp Fire where many residents were forced to drive long distances to see a doctor,” Beard said.

The Opportunity to Lead

Health insurers can take the lead on climate change in several ways.

For instance, the Boston Consulting Group suggests that “Insurers should collaborate with climate research and university institutions and should assist governmental and academic institutions in climate-health policymaking discussions.”

Health plans can look to create new insurance products and specified insurance models to address climate change health effects. Payers can explore implementing wider disease coverage and climate specific products. Looking to other countries may also help in generating new ideas. For example, Japan has implemented heatstroke insurance in response to climate change, costing members roughly 70 cents a day; in a single day they sold about 7,000 policies in June 2022.

Payers should also focus on underserved populations, as these groups often experience the worse climate change effects while contributing the least to pollution and carbon emissions. Collaborating with other institutions and agencies could be beneficial in this implementation.

Payers can also look to generate new opportunities by establishing health services that go beyond insurance. Climate change is already having an impact on payers’ portfolios, and this is a great way to diversify. Partnering with private equity firms to expand care delivery and creating tools for optimizing emergency-room triage and resource allocation are a couple of options that payers can explore.

The COVID-19 pandemic brought about several CMS waivers that aimed to expand telehealth access and coverage. Now we’re seeing those waivers that were set to expire at the end of 2024, extended.

The House Ways and Means Committee has voted to advance the Preserving Telehealth, Hospital and Ambulance Access Act (HR 8261) which would continue pandemic-era CMS Medicare waivers for telehealth access and coverage through 2026. It would also extend the CMS Acute Hospital Care at Home waiver for an additional five years, to the end of 2029.

While there is support for having these waivers be made permanent, for now a new bill would extend the telehealth waivers for two years and the Hospital at Home waiver for five years.

A few policies in this bill include: allowing Medicare patients to continue to receive telehealth services in their home, no geographic restrictions for originating sites for telehealth services, and allowing the use of audio-only communication platforms.

Many CMS waivers that were set to expire in 2024 are being extended.

The Centers for Medicaid and Medicare Services have extended the flexibilities designed to help states keep eligible individuals enrolled in Medicaid through June 2025, revising the initial expiration set for the end of 2024.

The waivers were originally set to expire by the end of 2024, but will be extended for six more months, according to a memo to states written by deputy CMS administrator and director of the Center for Medicaid and CHIP services Daniel Tsai. Other unwinding-related section waivers will be extended through June 30, 2025

According to a memo to states written by deputy CMS administrator and director of the Center for Medicaid and CHIP services Daniel Tsai, many states were expected to finalize the Medicaid unwinding process by June of 2024. However, due to several state extension waivers from CMS, several states will continue renewals past this date.

Loss of Coverage

Originally, HHS estimated that roughly 15 million individuals would lose Medicaid coverage. According to KFF news, over 21 million individuals have been disenrolled from Medicaid since April 2023.

Of that number, around 69% were disenrolled for procedural reasons, for example, not returning mandatory paperwork; not because they were ineligible for the program. The total Medicaid/CHIP Enrollment as of March 2023 was 94 million individuals, almost a third of the national population.

CMS looked at this massive volume of renewals following resumption of normal operations and called for the states' use of the timeliness exception to delay procedural disenrollments. This gave states time to conduct targeted outreach to encourage beneficiaries to return the renewal form.

CMS has approved a total of 398 waivers 52 states and territories, including Puerto Rico and the U.S. Virgin Islands. The waiver uptakes varied greatly by state: South Dakota requested a single waiver, while Indiana and Tennessee requested 15 each.

CMS also noted that this extension of flexibilities to streamline renewals will enable states to shift limited resources to reduce processing time at application when needed.

Payers

Health plans have faced much scrutiny as Medicaid unwinding moved along, and many payers still profited. Initially, payers said they expected the overall risk profile of their members to go up, due the fact that those remaining in the program would be sicker.

During the pandemic Medicaid enrollees’ health costs were lower, and several states made the decision to exclude pandemic-era cost data as they moved to set up payment rates for 2024; which worked in the favor of Medicaid health plans.

According to KFF, there are still 24 million Medicaid beneficiaries awaiting states to determine eligibility.

UnitedHealth continues to make headlines months after the cyberattack.

UnitedHealth has remained in the news since the Change Healthcare cyberattack earlier this year.

CEO Andrew Witty recently testified in front of the Senate and provided some updates surrounding the attack—including how it happened—the details of UnitedHealth Group’s (UHG) security controls. Witty also stated it was his decision to pay the large ransom.

From the initial cyberattack, to lawsuits, to divestitures; here are five updates on UnitedHealth Group.

Left without cost data, a study shows employers are still struggling to create better health plans.

A new report published by RAND found that during 2022 private insurers paid hospitals on average 254% of what Medicare would have paid for both inpatient and outpatient services.

Looking at the information from over 4000 hospitals in 49 states, the report showed that private health plans were paying more for the same services; despite wide price variation according to state.

While the number of hospitals and insurance claims has grown, the state-level average price remains 200% greater than Medicare prices.

In 2022, prices for inpatient hospital services averaged 255% higher than Medicare prices, outpatient services averaged 289% higher, and other professional services averaged 188% higher. Even prices for common outpatient services swelled, averaging 170% higher than Medicare payments.

The report estimates that about 160 million Americans have private health insurance, and these hospital increases are key growth drivers in per capita spending.

Drug Costs

When the study weighted each state’s prices equally, researchers found that commercial insurance prices for “select administered drugs received in a hospital setting averaged 278% of average sales price, compared with 106% of average sales price paid by Medicare.”

Payers, Prices and Data

This issue of price transparency isn’t new to the health insurance landscape. Employers have often struggled with creating well-structured plans.

Although federal policies require hospitals to post some prices for “shoppable” services and for insurers to post full sets of negotiable rates, many have not complied. Another issue here is that insurer data often contains duplicate information that inflates the file size, making it difficult to use.

“The widely varying prices among hospitals suggests that employers have opportunities to redesign their health plans to better align hospital prices with the value of care provided,” said Brian Briscombe, who currently leads the RAND hospital price transparency project.

“However, price transparency alone will not lead to changes if employers do not or cannot act upon price information.”

Krishna Ramachandran, senior vice president of health transformation and provider adoption at Blue Shield of California, spoke of the efforts that his organization has made to combat these cost pressures. This includes a collaboration amongst the Office of Health Care Affordability, Pharmacy Care Reimagined efforts, and Pay for Value and Data Exchange solutions.

“We also acknowledge that the healthcare system is getting increasingly complicated, and many parts of this fragmented system are left scrambling to manage a variety of care for all age groups, which this RAND study helps highlight,” Ramachandran said.

Insurers should work with employers to distribute accurate data to combat this issue. We saw a back and forth over this issue in February. Often, employers and plan sponsors said that insurers were refusing to hand over their claims data, which even led to some federal investigations.

The report presented a significant win for hospitals, yet illustrates where more funding is needed.

The Medicare Trustees Report shows that the Hospital Insurance Trust Fund is in better shape than we previously thought. According to the report the program will be able to pay all scheduled benefits until 2036 - seven years later than what was reported in 2023.

All parts of Medicare are expected to grow over the next couple of decades, and reforms will be needed to ensure a slowing of that growth and build revenue for the trust fund.

Although the report did cite some greater financial issues, the Biden Administration seems pleased with the results, seeing it as a correlation of the administration’s focus on economic and healthcare policies such as the Inflation Reduction Act.

The upswing of the Hospital Insurance Trust Fund is attributed to a policy change of how medical education costs are calculated for Medicare Advantage rates in 2024. The result is greater payroll tax income from an economy that performed better than economists had expected, as well as lower 2023 costs for inpatient hospital and home health agency services.

“The Biden-Harris Administration has left no stone unturned in our efforts to strengthen and preserve Medicare, not just for our parents and grandparents but for our children and generations to come,” said Department of Health and Human Services Secretary Xavier Becerra in a statement. “We will continue this work by negotiating the cost of prescription drugs, ensuring no one with Medicare goes bankrupt paying for lifesaving prescription drugs.”

Physician Payments

One major problem that is still lurking is physicians payments, the report citing that trustees expect “access to Medicare-participating physicians to become a significant issue in the long term.”

Many groups agreed, including lawmakers from the Medicare Payment Advisory Commission (MedPAC) and Jesse Ehrenfeld, M.D., president of the American Medical Association.

“This report continues the drumbeat of recommendations that all point out that the payment system is failing patients and physicians," Ehrenfeld said in a statement. "It would be political malpractice for Congress to sit on its hands and not respond to this report."

Physician payments have decreased roughly 30% since 2001, a major problem for underserved providers.

While MedPac agreed that physician payments should be higher, its report that was released in March capped its inflationary update at 50% of the Medicare Economic Index for physician services in 2025. Many groups such as AMA and AHIP slammed the organization for not doing enough to address the issue.

The added years to the Hospital Insurance Trust Fund are a significant improvement, but there is still much work to be done in terms of long-term stability in the healthcare industry. The report suggests two potential solutions: raising the payroll tax from 2.9% to 3.25% or reducing expenses by 8%.

We will have to check back on this issue to see which, if any, solutions will play out.

Implementing innovation and new ideas in health systems can be a tricky endeavor. With tight margins and increasing competition, new innovation strategies must be creative and flexible.

Atlantic Health System has implemented an innovative venture capital strategy, complete with a venture studio. Doug Hayes, the studio’s executive director, says health systems need to focus on the pursuit of their own innovations, instead of looking elsewhere for ideas or guidance. The New Jersey based health system has created a four pronged approach when it comes to innovation.

Payers are shifting their priorities in the MA space.

Medicare Advantage often takes the spotlight and next year will bring about some big changes that are sure to keep it there. Payers were up in arms over Medicare Advantage base rate cuts that will drop to 0.16% in 2025. Payers fought for higher payments, but CMS finalized this rule in April.

With this lower reimbursement rate and high medical costs, some payers are adjusting their strategies and looking at profitability and margins over membership growth.

Atena is looking to implement this strategy as it pulls out of less profitable counties. With disappointing first quarter results, Aetna CEO Brain Kane said the company will prioritize profitability over membership growth.

“It's hard to say right now that we won't have a meaningful decrease in membership," Mr. Kane said. "It's certainly possible."

Humana is also looking to exit some markets next year after examining its first quarter results. According to The Wall Street Journal, Susan Diamond, Humana's CFO, said the company is expecting a net decline in its MA membership next year.

Some insurers have also said they will cut back on supplemental benefits due to the rate cuts, which was an adjustment we all saw coming as payers scrambled for new ways to cut costs after disappointing MA numbers.

CVS Is another payer looking to readjust. CVS Health CEO Karen Lynch said it will adjust plan-level benefits in 2025. Supplemental benefits like fitness reimbursement could be on the line.

0b3c.jpg?itok=wkmTDzMy)

8346.jpg?itok=u8H1U4ae)

.jpg)

b063.jpg?itok=Ggrkr8z3)

.jpg)

10bb.jpg?itok=FHy65UU3)