"We are not going to leave dollars on the table," CFOs say.

During a panel at last week’s HFMA Annual Conference in Las Vegas, CFOs discussed pain points they’re currently facing and emerging opportunities.

Topics ranged from action plans for addressing industry challenges to examining current financial trends that are impacting healthcare, but there were three specific areas where CFOs seem to be placing their focus.

Artificial Intelligence

One of the first trends spoken about was the implementation of artificial intelligence. CFOs voiced concerns about the governance of AI and how smaller organizations are having trouble implementing it. Some brought up the need for an ‘automation road map’ to serve as a guide, and the importance of a such a plan for every health system.

“We’re starting to dip our toes in, but it’s a slow process,” said Jana Cook, CFO of Phelps Health.

Perhaps this is something that every leader should keep in mind. The consensus was that AI implementation is a process that needs to be taken slow with the right type of governance in order to do it successfully.

Big Pharma

Big pharma’s impact on health systems was the next topic of conversation, with panelists and attendees discussing the 340B drug pricing program and the significance of improving the cost of pharmaceuticals.

“Pharma and the health plans are winning right now,” Robin Damschroder, executive VP and CFO of Henry Ford Health System said. “They’re winning in the battle of who is doing better in the community.”

Hospitals and health systems face a great financial burden as drug companies increase prices.

While drug manufacturers are trying to lobby against the program, Damschroder stressed the need for health systems to push back against big pharma efforts and the importance of coming together to speak with one voice.

In order to do that, Damschroder said, it will take a collaboration of colleagues at the individual professional associations within the different physician specialties to come together.

Payer Pains and Denials

Commercial payer denials are coming in at an alarming rate for many health systems. One study cited that commercial payer denials for inpatient and outpatient services increased to 15.1% in 2023, compared with 3.9% for Medicare in the first quarter.

One of the biggest changes the group spoke about was going from commercial pay to government pay. One CFO discussed the how their organization dealt with denials by implementing weekly payer meetings and putting an emphasis on documentation coding, calling it “long, hard, steady work.”

The HFMA Annual Conference tackled all things finance this year, but one area that seemed to dominate discussions? The revenue cycle. From payer woes to strategy improvement, here are a few key trends that were top of mind at the event.

Payers Aren’t Playing Nice

No big surprise here: payers are playing by their own rule book.

Almost every discussion at HFMA this year mentioned payers in some capacity. That’s because they’re causing more issues for health systems than ever before. Denial rates have been increasing year over year, and reimbursement can take up to three months or longer.

Heavily capitalized payers are becoming more and more common, and they’re often playing hard with health systems, from using AI to inaccurately automate denials to bringing reimbursement to a stand-still.

Several sessions spoke about the importance of partnering with the right payers and emphasized the importance of transparency in these partnerships.

Executive leaders said don’t be afraid to go out of network and use other hard ball tactics to push back on payers.

You need systemwide revenue cycle participation

With revenue cycle management being a major topic this year, executives shared what is working at their health systems.

One session discussed the importance of the relationship between CFOs and the revenue cycle team.

There must be a certain level of trust in this relationship in order for both departments to thrive. CFOs should not have to micromanage the revenue cycle but should be there for guidance and eliminating barriers.

One session discussed the concept of physicians being more involved in revenue cycle decisions. Afterall, physicians are the ones with the medical degree and are the ones experiencing the operational issues firsthand in their work.

RCM has a lot of room for improvement, and hope is not a strategy

Just about everyone thinks they have the solution to revenue cycle problems.

The reality is there is no one size fits all solution and executives will have to examine the specific needs of their organization to identify opportunities for improvement.

Often, health systems rely on dozens of vendor support to manage their revenue cycle. One study presented at a session cited that the average health system uses about 40 vendors to support RCM efforts.

There’s a number of solutions and support out there, but finding the right one will take meticulous tracking of revenue cycle. “Hope is not a strategy,” said one CFO during a session.

A few leaders shared their insights on where they think the revenue cycle may be five years from now, saying that the department will likely be far more automated. But leaders warned to not get too carried away.

Standard processes shouldn’t be automated, many said. Revenue cycle teams should look towards investing in the right technology to improve RCM efforts and ensure that the technology benefits the specific mission-critical components of their organization.

Reimbursement and growth strategies are at the forefront of the CFO's role and says it's the future for CFOs.

Colleen Blye took on the role of executive vice president and CFO for New York-based health system Montefiore in 2016. Now, she's taking on the role of chief business officer.

Blye recently stepped into her added role, describing it as “very exciting,” she believes that it’s where all CFOs are heading.

“The intersection of finance along with organizational performance and strategy is what allows us to truly execute strategically to be financially sustainable,” Blye told Healthleaders.

Montefiore is comprised of 10 hospitals and more than 200 outpatient ambulatory care sites. Working with an incredibly diverse population, Blye spoke about the forethought and strategy that goes into making decisions for the health system. She dove into some of the biggest pain points her organization faces, including government reimbursement.

“Across our footprint, [...] we are always making sure to invest where the needs are and to re-position as healthcare evolves,” she said.

“Today, we grapple with doing all of this in an environment where reimbursements don’t always cover the cost of care. As an organization serving 85% government payor, 50% of our revenue comes from the 15% of our patients who have commercial insurance.”

Blye noted that while the regulatory environment and resources allocations are well intentioned, it can result in reimbursement delays and, ultimately, gaps in care.

Strategic Growth

Despite reimbursement woes, Blye is focused on Montefiore’s growth, and the strategy includes academically pushing the boundary. Montefiore stands as a leading academic medical center with a focus on clinical care and academic research.

“They go hand in hand and, at the end of day, we’re making advancements in the field of science, and our communities benefit from our work,” she said.

“Looking for sound business opportunities to help us continue pushing these boundaries is what I’m most excited about.”

Blye’s new role also has her overseeing the systemwide initiative to position Montefiore Einstein for growth and sustainability.

“Our transformation work is focused on our future. We are thinking about how we can continue to meet our patients’ expectations while grappling with growing inflation, labor costs and the ever-changing financial dynamics of healthcare,” she explained.

“Transformation allows us to think big, looking across disciplines within the system to evaluate and prioritize for the long-term.”

Looking ahead, Blye says that while healthcare economics are complicated, nuanced and ever-changing, she is tuned in to one two-part question as she moves forward: “How do we ensure the delivery of care and what is the future economic model of healthcare?”

Payers can successfully negotiate if they can prove they can stabilize finances.

The tug-of-war between payers and providers hits the precipice at the negotiating table. Contract negotiation is more than just tough business, and the strategies each party takes to the table can be do or die for any organization.

Before going into a negotiation, both payers and providers need to put in some research.

For example, providers must ensure they’ve reviewed their contracts and create a habit of doing so often. On the other hand, payers must also ensure they are up to date on their contracts and can supply providers with accurate information and data throughout the negotiation process.

When it comes to successful negotiations though, proving that you can help reduce expenses is an important strategy for payers to utilize.

How to Show That You Can Reduce Expenses

Payers can successfully negotiate if they can prove they can stabilize finances. Although most healthcare leaders on both sides are optimistic and expect financial performance to improve, a few key areas will push them to do so.

“Rising labor costs in healthcare and a substantial increase to the regulatory and legislative mandates are driving increased costs for both providers and health plans,” said Krishna Ramachandran, Blue Shield of California’s senior vice president of health transformation and provider adoption.

Payers and providers will need to collaborate and examine specific avenues that health systems can take to reduce expenses to have a portion of the funds returned to their organization.

Both parties can bring up digitization, which can play a large role in the negotiation: from utilizing AI to reduce administration workload, to implementing EHRs to reduce paperwork and streamline operations, leaders must examine options that work for their system. Payers can cut costs and pass savings onto their organization; this is beneficial to both parties.

For payers this is important because the less the administrative cost, the better for everyone, Piyush Khanna, vice president of clinical services at CareFirst Blue Cross Blue Shield, explained, agreeing that AI has the potential to help, but must be done responsibly.

Part of that responsibility goes back to ensuring accurate data sets; technology will only be as good as the data. “The data backbone is extremely critical for these statistical models of the future to be able to leverage this information,” Khanna said. “These tools need good, curated data sets [in order to] to be meaningful.”

But health leaders should not only look to the newest digital solution to fix their problems. Digital tools and programs must be integrated in a way that best paves the road to success for that specific organization.

Ramachandran stated that to drive tangible change, industry leaders must provide solutions that are proactive and integrative, giving an example of how Blue Shield is investing in tools and partnerships to bring healthcare into the digital age: “This includes tools to streamline data exchange between providers and health plans so that we can reduce the burden of administrative transactions and focus efforts on member health.”

Private equity bankruptcies are projected to increase in 2024.

Private equity is woven into many health systems, and it’s not always playing out well. According to a new report by the Private Equity Stakeholder Project, health systems funded by private equity have entered a pattern of financial distress and bankruptcies. The report notes that 2023 marked a record year of large healthcare bankruptcies, and private equity accounted for some of the largest ones.

According to the findings, this wave of financial distress is projected to continue throughout 2024 as many organizations face credit rating downgrades and potential defaults. Most of the companies at risk are owned by private equity. This raises questions about private equity's place in healthcare, as well as CFO strategies and care outcomes. Taking this evidence into consideration, CFOs should look at weighing the pros and cons of private equity and if it truly is helping an organization move forward towards its financial and clinical goals.

The healthcare expenditure forecast is outpacing just about everything.

Healthcare spending is soaring and is expected to climb even higher over the next eight years. But the impact will be felt in places other than the consumer’s wallet.

Two new reports: The CBO National Health Expenditure Forecast to 2032, and The Bureau of Labor Statistics CPI Report for May 2024 and Last 12 Months (May 2023-May2024) are predicting significant increases in healthcare spending through 2032.

According to the CBO, which forecasts major increases from 2024 to 2032, the National Health Expenditure is expected to increase a whopping 52.6%, jumping from $5.048 trillion to $7,705 trillion, claiming 17.6% of the GDP. The NHE/Capita will increase 45.6%, taking it from $15,054 in 2024, to $21,927 in 2032.

Other major categories will also see a big jump: Physician services spending is expected to increase 51.2%, making up 19.7% of total NHE, and hospital spending also will accelerate to 51.6%, jumping to 30.7% of total NHE.

Two other categories are also set to jump: Prescription drug spending and net cost of insurance. Prescription drug spending will increase 57.1%, taking it to $728.5 billion, while the net cost of insurance will increase 62.9%, escalating it to $534.7 billion.

Medical services, which increased 3.1%, represent about 6.5% of the overall Consumer Price Index, but there is much variance among spending categories. Notably, hospital and over-the-counter prices exceeded the overall CPI. Hospital services were at 7.3% over the last year, (1.0% of the CPI total), and OTC prices were at 5.9%.

What does it all mean for the industry?

While the healthcare economy is large, and only expected to get larger, Paul Keckley notes that, outside of OTC products, consumers aren’t the ones who will notice the increase of expenses. Employers and state and federal governments who fund the majority of healthcare spending will feel the brunt of these increases.

Hospitals and physician services are expected to remain the same, he says, but prescription drugs and health insurance will increase. As these increases draw in more attention to price control methods, tensions between payers and providers will likely rise. These two parties will need to pace towards innovative price control practices to smoothen out negotiations around spending.

According to Keckley, there isn’t much to indicate that value-based care has lowered spending in any notable way, nor is it considered significant in these forecasts.

For value-based care to truly have an impact on healthcare spending, hospital executives and payers will need to work together to examine what types of value-based care models will create an impact specific to their organization. And while this type of care is fondly spoken about among health executives, implementation will require strategic plans in order to be beneficial to the industry.

As healthcare spending expands above the GDP, population growth rates, and overall inflation, Keckley says it may not be sustainable.

“Its long-term sustainability is in question unless monetary policies enable other industries to grow proportionately and/or taxpayers agree to pay more for its services. These data confirm its unit costs and prices are problematic,” Keckley says.

CFO Doug Watson shares what is top of mind as he officially steps into his new role at Allina Health.

Allina Health, a Minnesota-based health system, just named Doug Watson its new chief financial officer.

Watson stepped into his new role in June, having served as interim CFO. He brings a wealth of finance experience to his position and has some goals in mind for the system.

Luckily for Watson he is more than well-suited to tackling his top-of-mind issues and goals as he moves forward in his organization. He previously served as Interim Executive Vice President and System CFO at Sharp Healthcare, as well as several other vice president and CFO roles.

Labor Expenses

Labor currently makes up about 60% of average hospital expenses, and Watson notes the aging population’s potential to exacerbate the issue.

“When you see the population of the country aging into a higher level of needed care, that's challenging in an environment where staffing is really difficult,” Watson told HealthLeaders. “We're not minting enough nurses or doctors to keep up with current demand.”

The healthcare industry has been in a balancing act with commercial insurance underpinning the subsidization of government programs over the last few decades. Watson thinks that may change with a growing aging population.

“When you're a senior citizen, you want to access care differently than you did when you were younger,” Watson said. “As you start shifting the demographics, it really starts to challenge that historic balance and it's unclear how that's going to work out.”

The Patient Experience

Another top-of-mind goal for this CFO? Creating a friction-less patient experience.

Watson says friction comes into play for a patient when they aren’t in the know. Regardless of a system’s care model, he says the key is to be looking to produce care at an affordable cost point, in the right setting, at the right time, in a manner that is patient friendly.

“I think there's a lot of opportunity to improve that and that's certainly one of the things we're thinking about,” he said. “How do you think about the patient journey, and where those points of friction are? Where are those opportunities, where they're directly related to us, that we can change?”

Going forward, Watson is looking at how leaders can make healthcare "more efficient, effective, and friendly.”

Will health systems begin to steer clear of private equity investments?

Private equity is everywhere. As it continues to be a controversial topic, the Steward Health Care fiasco has made that spotlight even brighter.

As Steward Health Care is on its way to securing a $225 million loan to keep its 31 health systems operational ahead of auctions, its actions have not gone unnoticed by lawmakers.

The health system filed for bankruptcy on May 6 after it was days away from running out of money. Later this week Steward will seek approval for the loan, provided by a group of unidentified lenders, in bankruptcy court. The loan is expected to keep the health system running until autumn.

According to a WBUR report, Steward has said that it has more than 100,000 creditors and liabilities lying somewhere between $1 billion and $10 billion.

Massachusetts state officials are fed up with the health system, claiming it has threatened public health across the east side of the state. In February Massachusetts Governor Maura Healey and House Speaker Ron Mariano demanded for Steward to reveal its finances, sell its hospitals and leave the state completely.

Steward plans to sell off its remaining hospitals and physicians’ network at a pair of auctions on June 27.

Legislation Inspiration

A new bill is aimed at preventing future Steward-like financial crises. The Corporate Crimes Against Health Care Act proposed by Senator Elizabeth Warren is aimed at cracking down on private equity misconduct in healthcare. The bill would pose high penalties for investors who profit at the expense of their healthcare business.

According to a report from the Boston Herald, Warren, along with the president of the Massachusetts Nursing Association and other healthcare workers, Steward’s CEO and equity firm Cerberus made millions by purchasing hospital properties, selling off the land underneath the buildings and then leasing the buildings back to the hospitals.

“Let me be clear, this disaster is private equities’ fault. Cerberus and Steward’s CEO Ralph de la Torre, cut Steward’s resources so close to the bone that hospitals couldn’t afford lifesaving medical care,” Warren said, according to the report.

Warren said the proposal would not inhibit Steward’s bankruptcy proceedings, but it would prevent other health systems from taking the same path of ownership via private equity.

The proposal would make it a crime to steer a hospital towards bankruptcy to the point where a patient dies. Health system CEOs could be charged with manslaughter and face a prison sentence under the plan.

The Future of Private Equity

Healthcare bankruptcies related to private equity have been on the rise, but new findings reveal that actual investment activity by firms continues to slow down. A handful of factors come into play here including buyer and seller price differences, regulatory climate and hints that the Federal Reserve will hold rates higher for longer.

As the healthcare industry continues to pump the brakes on private equity, coupled with Warren’s proposed plan, private equity may even come to more of a lull in the future. Much is still yet to be determined, including the approval of Warren's plan and the financial viability of Steward Health for the rest of 2024 and beyond.

Accurate payer-provider data exchange is critical to negotiations. If one party does not have plentiful, accurate data, it can hurt everyone involved.

The tug-of-war between payers and providers hits the precipice at the negotiating table. Contract negotiation is more than just tough business, and the strategies each party takes to the table can be do or die for any organization.

Before going into a negotiation, both payers and providers need to put in some research.

For example, providers must ensure they’ve reviewed their contracts and create a habit of doing so often. On the other hand, payers must also ensure they are up to date on their contracts and can supply providers with accurate information and data throughout the negotiation process.

When it comes to successful negotiations though, leveraging data is an important strategy for payers to utilize.

Let Data Drive the Discussion

Both payers and providers should know their target statistics, both financial and strategic, and how they need to be adjusted. If each party comes amply prepared with data, it makes it easier to see where the numbers, like KPIs, protocols, and evidence-based medicine data sets need to fall. Each should ensure that they understand their data, the key issues for their organization, and the solutions that will be viable for both parties.

When it comes to the payer’s role in data, Piyush Khanna, vice president of clinical services at CareFirst Blue Cross Blue Shield, says payers can help provide accurate data for providers so they can look at information in the same way payers do.

“When we go into the negotiation we can put that data in front of [the providers], but we need to also make sure they have access to it throughout the contracting process, so they have more real-time intervention capabilities to influence patient outcomes,” Khanna said.

With higher use of EHRs and more clinical data repositories available to both the payer and the provider, Khanna said that the data is there, but it can be unorganized and slow to make an appearance.

“We can certainly leverage the power of the data, and we have to remember data has been traditionally fragmented in healthcare,” Khanna said.

“I think clinical data access in more real time will become more relevant. Because whether it's progression or regression on outcomes, you want to have more leading indicators that are available through the clinical data set. That is something I see as more leveraging and making it into contractual aspects as well, especially on readmissions.”

While data that reflects the needs and goals of each organization is highly important, data that reflects cost utilization and expense can truly drive the discussion home. At the end of the day each health care leader involved knows that sustainable profitability is crucial to keep an organization in business.

Stepping into the negotiation room with an open mind, hard numbers, and flexibility will be vital, no matter which side of the table you are on. The more data, the better. If you are approaching the negotiation table with exact numbers, you’ll be able to articulate exactly where your organization can be flexible, and where it cannot.

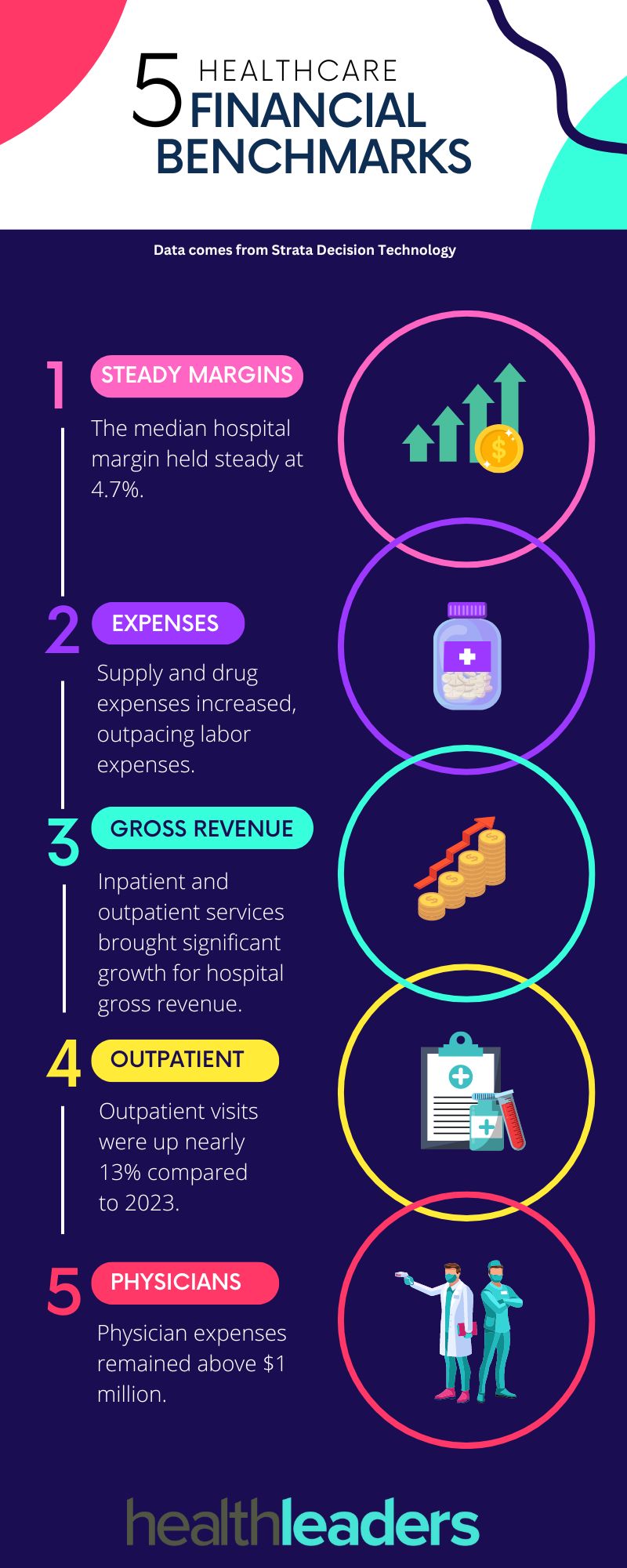

A new report by Strata highlights the latest financial performance for hospitals and physician groups across the country. The report, which looked at monthly data from over 135,000 physicians and 1,600 hospitals, highlights five key metrics.

The median hospital margin held steady for a second month at 4.7%, while patient volumes and revenues continued to increase.

Supply and drug expenses for hospitals increased, which put non-labor expenses ahead of labor expenses after a slowdown the previous month.

Both inpatient and outpatient services brought significant growth to gross hospital revenues and hospitals saw a 12th consecutive month of year-over-year gross revenue increases.

The highest year-over-year in patient volumes came from outpatient visits which were up almost 13% compared to the same time in 2023.

Physician expenses stayed above $1 million in April and physician practices continue to generate high costs in need of investment support for practice operations.

a73a.jpg?itok=bhjnbyB7)

.jpg)

.jpg)